So, you're standing in front of a beautiful old building, one with character, history, and incredible potential. But when you start running the numbers on a renovation, the costs can feel overwhelming. This is exactly where historic preservation tax credits come into play, turning what seems like a daunting project into a smart financial move.

Turn Historic Buildings into Profitable Ventures

These credits aren't just some minor tax break; they are powerful incentives that can dramatically lower your project costs. This guide will walk you through how combining federal and state programs can unlock the full financial potential of a historic property. It’s more than just restoration—it’s a strategic business decision that can seriously boost your return on investment.

Think of it this way: a tax credit isn't a simple deduction that just lowers your taxable income. It’s a direct, dollar-for-dollar reduction of the taxes you actually owe. It’s like having a financial partner in the project, making the restoration of architectural treasures not just possible, but often highly profitable.

A Proven Engine for Economic Growth

The ripple effect of these incentives goes far beyond a single project's bottom line. Since it kicked off in 1976, the Federal Historic Preservation Tax Credit (HTC) program has become a true powerhouse for community revitalization. It has sparked over $235 billion in private investment to bring more than 48,000 historic properties back to life.

For developers working with experienced firms like Sherer Architects, this program is a key tool for turning fading landmarks into thriving, profitable assets.

What’s really compelling is where these projects happen. A staggering 78% are in economically distressed areas, 50% are in low- to moderate-income neighborhoods, and 29% are in small communities. This isn't just about saving buildings; it’s about directly tackling urban decay and breathing new life into rural towns.

More Than Just Preservation

At its heart, this is a program about smart, sustainable development. By using historic preservation tax credits, you’re doing much more than just fixing up an old building. You can:

- Boost Your ROI: The credits directly lower your project costs, which naturally increases your final return on investment.

- Enhance Community Value: Revitalized buildings create jobs, bring energy back to neighborhoods, and adapt unique structures for modern commercial use.

- Access More Capital: When you walk into a bank with approved tax credits, your project instantly looks more financially sound to lenders and investors.

To get the most out of these opportunities, it's wise to weave these credits into a broader set of real estate investment tax strategies. By understanding how to navigate the process, you can transform architectural treasures into profitable, community-enhancing assets.

Combining Federal and State Tax Credits

The real magic in financing a historic renovation isn't just finding one tax credit program; it's learning how to stack them. Think of it as building a financial engine with multiple, powerful parts. You don't just use the federal program or the state one—you combine them to create a much more substantial, profitable outcome for your project.

This strategy is especially potent here in South Carolina. We have a fantastic state-level program that dovetails perfectly with the long-standing federal credits. By understanding how these two systems work together, developers and property owners can dramatically cut their out-of-pocket costs and tax burdens, turning what might seem like a passion project into a truly smart investment.

The Foundation: The Federal Historic Tax Credit

The bedrock of this strategy is the Federal Historic Tax Credit (HTC). This is the big one, but it’s designed specifically for income-producing properties. If you're bringing a commercial building back to life, converting an old warehouse into lofts, or renovating a rental property, this is where you start.

The federal program offers a 20% tax credit on your Qualified Rehabilitation Expenses (QREs). And let’s be clear: this isn’t a deduction. It's a direct, dollar-for-dollar reduction of what you owe in federal income taxes. If your project has $1 million in eligible costs, that’s a $200,000 credit in your pocket. That kind of number can completely change the financial viability of a project right from the get-go.

Of course, this incentive comes with high standards. You have to follow the Secretary of the Interior’s Standards for Rehabilitation, but for those who plan carefully, the financial reward is more than worth the effort.

South Carolina's State-Level Power-Up

While the federal credit is a game-changer on its own, South Carolina’s own incentives are what make stacking so incredibly lucrative here. The state actually offers two different historic tax credits, which opens the door to more than just commercial developers.

- For Income-Producing Properties: For these projects, South Carolina adds a generous 25% state income tax credit on top of the federal one. This stacks directly with the 20% federal credit, giving you a combined 45% of your costs back in credits. That synergy is powerful enough to make almost any historic project financially compelling.

- For Owner-Occupied Homes: Here’s where South Carolina really stands out. Unlike the federal program, our state also offers a 25% state income tax credit for homeowners who rehab their personal historic residence. This is a fantastic opportunity for individuals to preserve their own piece of history and get a significant financial benefit for doing so.

This dual-pronged approach makes South Carolina one of the best places in the country for historic preservation. The combined federal and state incentives create a financial package that’s tough to beat.

Imagine you're a developer in Charleston or Columbia looking at a $2 million rehabilitation. Stacking the 20% federal credit ($400,000) with the 25% state credit ($500,000) gives you $900,000 in tax credits. That’s nearly half the project cost covered, which is often the key to getting a "yes" from lenders and investors.

Federal HTC vs South Carolina State Historic Tax Credits at a Glance

To really get a handle on how these programs work together, it helps to see them side-by-side. They’re designed to be partners, but they have their own distinct rules about property use, credit value, and ownership terms that you need to understand for smart project planning.

| Feature | Federal Historic Tax Credit (HTC) | South Carolina State Tax Credit |

|---|---|---|

| Credit Percentage | 20% of Qualified Rehabilitation Expenses. | 25% of Qualified Rehabilitation Expenses. |

| Eligible Properties | Income-producing only (commercial, industrial, rental). | Both income-producing and owner-occupied residential properties. |

| Minimum Investment | Rehab cost must exceed the building's adjusted basis (the "Substantial Rehabilitation Test"). | A minimum investment threshold applies, which varies by property type. |

| Recapture Period | A 5-year holding period is required to avoid credit recapture. | A 5-year holding period is also required for the state credit. |

This table really drives home the opportunity we have here in South Carolina. For commercial developers, the ability to combine these credits creates an incredible financial synergy. It maximizes the total return on investment and transforms the preservation of our state's beautiful historic architecture from a noble cause into a sound, profitable business strategy.

Does Your Renovation Project Qualify?

Figuring out if your project qualifies for historic preservation tax credits can seem daunting, but I always tell clients to think of it as a simple, three-part checklist. Before you get lost in the details of floor plans and budgets, we need to make sure your building and your project tick these fundamental boxes.

Think of it like this: there are three main gates you have to pass through to unlock the financial power of these credits. Each one looks at a different piece of the puzzle—the building's official status, the size of your investment, and the quality of the restoration work itself. Nailing these three things from the get-go is the most critical step you can take.

Is Your Building Historically Significant?

First things first, the building has to be officially recognized as historic. It's not enough for a building to just be old or have character; it needs a formal designation. This is the absolute, non-negotiable starting point for both the federal and state tax credit programs.

So, how do you know if your property makes the cut? It needs to meet one of two conditions:

- It’s individually listed on the National Register of Historic Places. This is the clearest path, meaning the building is considered significant all on its own.

- It's a contributing structure within a Registered Historic District. This means your building is a key piece of the neighborhood's historic fabric, even if it isn't a standalone landmark.

We can quickly help you verify your property’s status. If it's not yet certified as "contributing," we have experience guiding clients through that process.

Passing the Substantial Rehabilitation Test

Once you've confirmed the building's historic status, the next gate is all about the money. These programs are designed to reward major, transformative investments, not just a quick coat of paint or some minor updates. To qualify, your project has to pass the “Substantial Rehabilitation Test.”

It sounds technical, but the logic is straightforward: you have to spend more on the renovation than the building is currently worth.

The official rule is that your Qualified Rehabilitation Expenses (QREs) must be greater than the "adjusted basis" of the building. In simple terms, the adjusted basis is usually what you paid for the building (minus the land value), minus any depreciation you’ve claimed, plus the cost of any capital improvements you’ve already made.

Meeting this financial bar proves your project is a serious, significant undertaking. It's the government's way of ensuring the tax incentives go to projects that are making a real commitment to bringing these old buildings back to life.

Following the Secretary of the Interior’s Standards

The final gate is about the quality and sensitivity of the renovation itself. All the work you do must adhere to the Secretary of the Interior's Standards for Rehabilitation. A lot of people hear "standards" and think of rigid, stifling rules, but that’s not the case at all.

These ten standards are really just a set of best-practice principles for making smart design choices that honor a building's past while preparing it for a modern future. They guide everything from repairing old brick and windows to designing new additions, always emphasizing repair over replacement and ensuring new work complements the old. This is where an architect's experience is absolutely crucial. A firm like ours, that lives and breathes historic preservation, knows how to design a project that achieves your business goals while effortlessly aligning with these standards.

The ripple effect of these projects is incredible, often breathing new life into areas that need it most. It's no accident that half of all historic tax credit projects are in low-income communities and 78% are in economically distressed areas. These credits are a powerful engine for community growth. Exciting proposals are even on the table to make it easier for nonprofits to get involved, potentially allowing these credits to be combined with Low-Income Housing Tax Credits. You can learn more about how these incentives drive inclusive growth from this fact sheet from Preservation Action.

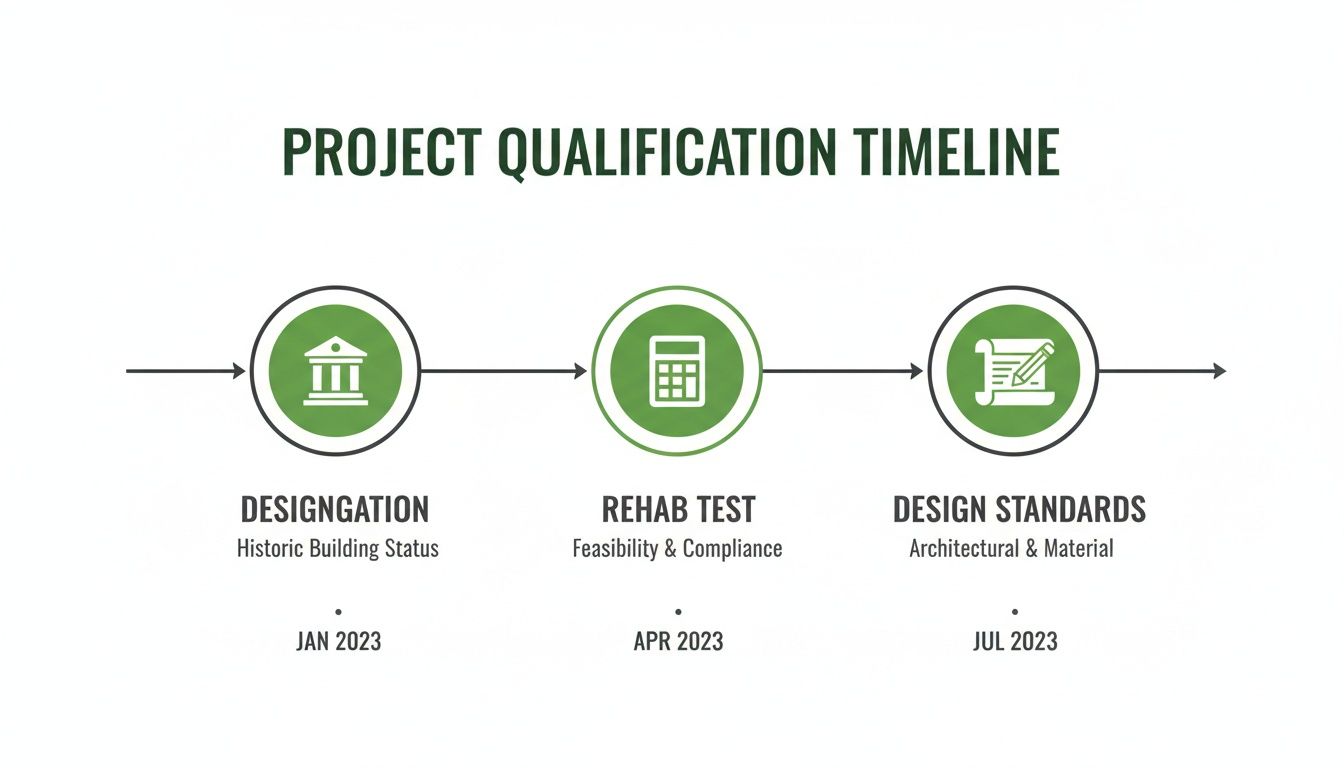

Navigating the Application Process Step by Step

Chasing historic preservation tax credits can feel like navigating a maze, but it's really just a straightforward, three-part journey. Think of the application as a story with a beginning, a middle, and an end. Each part builds on the last, and you have to complete them in the right order.

It’s a lot like building a house. You can't frame the walls (Part 2) until you've poured the foundation (Part 1). And you certainly can't get the final sign-off (Part 3) until the work is done. An experienced architect acts as your guide, making sure every document is filed correctly and on time, keeping the whole project on track from start to finish.

This timeline breaks down the three main checkpoints you’ll need to clear.

Each stage—proving the building's historic Designation, passing the Rehab Test, and following the Design Standards—is a non-negotiable step on the path to securing these credits.

Part 1: Certifying Your Building’s Historic Status

The whole process kicks off with the Historic Preservation Certification Application, Part 1—Evaluation of Significance. This is where you officially prove your building is worth preserving. Even if the property is already listed on the National Register, this step is required to get it formally recognized for your specific tax credit project.

Part 1 is all about documentation. You'll need to pull together:

- Photographs: Clear, current photos are a must. They need to show the building's overall condition and highlight its important architectural details.

- Historical Information: You'll write a narrative explaining the building's history and why it matters to the local historic district (if it’s in one).

- Maps: A simple map showing exactly where the property sits within the historic district.

Your architect will take this information and weave it into a compelling story for the reviewers at the State Historic Preservation Office (SHPO) and the National Park Service (NPS). Getting Part 1 approved is the green light that confirms your building is a deserving candidate.

Part 2: Getting Your Rehabilitation Plan Approved

Once your building's historic status is locked in, you’re ready for Part 2—Description of Rehabilitation. This is the heart of the application and, frankly, the most intensive phase. Here, you submit your full architectural plans and project details for review before you start any major work.

Let me be clear: this is a forward-looking step, not a look back. You're asking for permission, not forgiveness. The goal is to get the SHPO and NPS to sign off on your proposed work, confirming it follows the Secretary of the Interior’s Standards. Nailing Part 2 prevents expensive do-overs and frustrating delays later on.

A rock-solid Part 2 submission is your best insurance policy against project headaches. When it's put together by an architect who knows preservation inside and out, it shows reviewers you have a smart, respectful plan for bringing the building into the 21st century.

Part 3: Certifying the Completed Work

The final step is Part 3—Request for Certification of Completed Work. After the last nail is hammered and the paint is dry, you submit this application to show that the finished project matches the plans approved in Part 2. This is the finish line—where your project gets its final certification and the tax credits are officially unlocked.

This last package includes "after" photos that mirror the "before" shots from Part 1, plus a formal statement confirming everything meets the program's requirements. The NPS issues the final certification, which you then file with your income tax return to claim your credits.

Getting through these three stages takes foresight, an expert understanding of preservation rules, and constant communication with state and federal agencies. It’s a process where having the right professional in your corner isn't just helpful—it’s what protects your investment and turns your vision into a financial success.

How These Credits Impact Your Bottom Line

It’s easy to talk about percentages, but to really understand the power of historic preservation tax credits, you have to see what they do to a project's budget. These aren't just a nice little bonus; they completely reshape the financial DNA of a renovation, often turning a project that’s on the bubble into a fantastic investment. By directly cutting down your tax bill, these credits free up an enormous amount of capital and can seriously boost your return.

Let’s walk through a real-world example. The numbers really tell the story of how stacking federal and state credits can be the deciding factor between a project that just breaks even and one that’s a home run.

A Practical Case Study

Let's imagine a developer who has just purchased a historic warehouse in a part of town that's seeing new life. The purchase price was $800,000. The vision is to convert it into a mixed-use commercial space, and the budget for the full rehabilitation is $1,500,000.

First, we need to figure out the Qualified Rehabilitation Expenses (QREs). Think of these as the "hard costs"—the money spent directly on the building itself. This includes things like structural work, restoring original windows, or putting in new HVAC and electrical systems. In our scenario, the entire $1,500,000 budget qualifies.

Now, let's do the math on the credits.

- Federal Historic Tax Credit: The federal government offers a 20% credit on the QREs. For this project, that’s a $300,000 credit ($1,500,000 x 0.20).

- South Carolina State Tax Credit: Our state program offers an even more generous 25% credit. That adds another $375,000 to the mix ($1,500,000 x 0.25).

By combining these two programs, the developer gets a staggering $675,000 in total tax credits. And remember, this isn’t a deduction that just lowers your taxable income. It's a true, dollar-for-dollar credit that erases what you owe in future taxes.

Analyzing the Financial Impact

The effect of these credits goes way beyond that initial $675,000 figure. That savings changes the entire financial picture, making the deal far more secure and appealing from every possible angle.

Right off the bat, the project's net cost plummets. That $1.5 million renovation now effectively costs the developer only $825,000 out of pocket once the credits are accounted for. This drastically reduces the capital they need to raise and lowers the overall financial risk.

A project with nearly half of its rehabilitation costs covered by tax credits is fundamentally different from one financed entirely with debt and equity. It allows for a more conservative capital stack, better loan terms, and a faster path to profitability for investors.

This stronger financial footing creates a positive ripple effect. When you walk into a bank with approved tax credits, you're essentially showing them a form of secured equity. It signals that the project is not only financially viable but also has the backing of both federal and state preservation programs. This adds a layer of credibility that lenders love, often leading to better financing terms.

In the end, these historic preservation tax credits turn abstract ideas into tangible cash. They make projects more attractive to banks and investors alike, proving that saving our architectural heritage isn't just a good cause—it's smart business.

Why Your Architect Is Your Most Valuable Partner

When you kick off a project involving historic preservation tax credits, it’s natural to see your architect primarily as the person drawing up plans. But in this very specific arena, they are so much more. Think of them as your strategic partner, the person who safeguards your investment and makes sure your vision actually pays off.

Their job goes way beyond the blueprints. They’re your guide through the red tape, your advocate with review boards, and your quality control expert, all wrapped into one.

An architect who’s been down this road before—like our team at Sherer Architects—knows the process is a delicate dance. It’s about fitting modern needs into a historic shell in a way that checks all the boxes for the tax credit programs and for you. That kind of experience is what stops expensive mistakes before they happen and keeps the whole project on track.

Masters of Meticulous Documentation

The application for historic tax credits is a mountain of paperwork. And I mean a mountain. Every single detail is scrutinized. Your architect is the one responsible for creating the exhaustive documentation that the State Historic Preservation Office (SHPO) and the National Park Service (NPS) demand.

This isn’t just a set of floor plans. It’s a deep dive into the specifics:

- Detailed Drawings and Specifications: These aren't your average construction plans. They have to outline the exact methods and materials that will be used to repair or bring back historic features, from window glazing to masonry techniques.

- Comprehensive Photographic Records: A thorough “before” and “after” photo survey is non-negotiable. An experienced architect knows precisely what angles and details to capture to tell a compelling story of rehabilitation for the officials reviewing your file.

Getting this documentation right from the start is your first line of defense. It shows the review boards you’re serious and professional, leaving no room for questions or doubt.

Navigating the Secretary of the Interior’s Standards

The entire historic tax credit world revolves around one thing: The Secretary of the Interior’s 10 Standards for Rehabilitation. These are the commandments of preservation. A good architect doesn't just know them; they know how to interpret them creatively to solve real-world problems.

For instance, how do you install a modern, high-efficiency HVAC system without tearing apart the historic fabric of the building? How do you upgrade the electrical wiring to meet today's code while respecting original plaster walls? This is where an expert's guidance is absolutely essential to getting your historic preservation tax credits.

An architect’s true value is in being a translator. They translate your project goals into a language the government’s preservation requirements can understand, ensuring your design gets approved without killing your vision or your ROI.

This proactive approach to design saves you from soul-crushing (and budget-busting) revisions later.

Finally, your architect acts as your professional go-between. They handle all the communication with the SHPO and NPS, speaking their language and building the kind of rapport that makes the review process go smoothly. This constant advocacy protects your timeline and your bottom line, making sure your project successfully qualifies for every last credit it deserves.

Got Questions About Historic Tax Credits? We've Got Answers.

Jumping into a historic renovation project is exciting, but the financial details—especially tax credits—can feel a little daunting. It's completely normal to have questions as you try to line up your budget and timeline. We hear them all the time from developers and property owners just like you.

Let's clear up some of the most common points of confusion. Think of this as your go-to cheat sheet for navigating the process with confidence.

What Renovation Costs Actually Qualify?

This is the big one, right? It all comes down to what the government calls Qualified Rehabilitation Expenses, or QREs. Generally, this covers the hard costs of bringing the building back to life—things that are integral to its structure and function. We're talking about work on the walls, floors, roof, windows, and major systems like plumbing and electrical.

What's not included? Costs for buying the property itself, building a brand-new addition, or doing site work like paving a parking lot or landscaping. This is where an architect who knows the ropes is invaluable; they can help you meticulously categorize every expense to make sure you're maximizing every dollar of your potential credit.

What if I’ve Already Started the Renovation? Can I Still Get Credits?

Timing is absolutely critical here. Your entire rehabilitation plan needs the green light from both the State Historic Preservation Office (SHPO) and the National Park Service (NPS) before you finish the project. If you start swinging hammers and doing major work before getting that approval, you could lose your eligibility entirely.

It's a hard and fast rule: start the application process at the very beginning of your planning. The system is designed to approve a plan before work happens. Trying to get approval after the fact is a recipe for disappointment and a very expensive mistake.

How Long Do I Have to Own the Property?

Both the federal and state programs want to see long-term investment, not just a quick flip. That's why they have a five-year recapture period. If you sell the property within five years of completing the renovation (also known as "placing it in service"), you may have to pay back some or all of the tax credits.

The good news is that the amount you'd owe is prorated. It decreases by 20% for each full year you hold onto the property. After five years, you're in the clear.

Can I Get These Credits for My Own House?

This is a really common question, and the answer depends on which credit you're talking about. The Federal 20% Historic Tax Credit is designed specifically for income-producing properties. Think office buildings, retail storefronts, or apartment rentals.

But if you live in South Carolina, you're in luck. The state offers a separate 25% state tax credit just for owner-occupied historic homes. It's a fantastic incentive that helps homeowners invest in preserving the character of their own primary residence.

Ready to see how historic tax credits could make your next project's numbers work? The team at Sherer Architects, LLC lives and breathes this stuff. We can guide you through every single step, from figuring out if your building qualifies to getting that final certification. Let's talk about your project—get in touch with us today.