Before you even think about building, you need to answer one fundamental question: Will this project actually make money? A financial feasibility study is the tool that gets you there. It’s a hard-nosed, objective look at whether a real estate idea is economically viable, moving beyond gut feelings to a data-driven go/no-go decision.

This isn't just about crunching numbers. It's about stress-testing your vision against the realities of costs, revenues, and market risks.

Defining the Scope of Your Real Estate Project

Every successful financial analysis begins with a crystal-clear vision. Vague concepts like "a new retail space" just won't cut it. You need to draw a firm box around your idea, defining exactly what you want to build, who it's for, and the physical and financial constraints you're working within.

This step has never been more important. With business failures on the rise—the Bureau of Labor Statistics reports that 20.8% of businesses don't survive their first year—validating your concept is non-negotiable. Many of these failures happen because there was no real market need for the product. Your feasibility study is how you avoid becoming a statistic.

Gathering Your Core Inputs

To build a reliable financial model, you need to start with real-world data. These core inputs are the foundation of your entire analysis, and getting them right upfront saves you from costly rework and bad assumptions down the road.

Before you open a spreadsheet, you need to have answers to some critical questions:

- What can you legally build? This comes down to zoning and entitlements. You need to know the local height restrictions, setback requirements, parking ratios, and land-use rules.

- What are you building on? You'll need site-specific data from topography surveys, geotechnical reports, and environmental assessments (like a Phase I ESA). You don't want to discover contaminated soil or a high water table after you've already invested heavily.

- What will the building actually do? These are your program requirements. Define the gross square footage, the number of residential units or commercial tenants, and the specific amenities your target market expects.

A solid commercial real estate market analysis is the first, most crucial step. It helps you understand what the market wants, validating your program before you go any further.

To get organized, it helps to have a checklist of the data you need to pull together.

Initial Data Checklist for Your Feasibility Study

Here's a quick rundown of the essential information you'll need to collect before you can build a meaningful financial model.

| Category | Key Data Points | Example |

|---|---|---|

| Site & Legal | Zoning designation, allowable uses, height limits, setbacks, parking requirements, entitlements process. | "C-2 Commercial zoning allows for retail on the ground floor and 100 units." |

| Physical Data | Topography survey, geotechnical report, Phase I Environmental Site Assessment (ESA), utility maps. | "Geotech report indicates soil requires deep foundations, increasing costs." |

| Program & Market | Target market, gross square footage (GSF), number of units/tenants, proposed amenities, market rents. | "150-unit luxury apartment building with a pool, gym, and co-working space." |

| Existing Building | (For adaptive reuse) As-built drawings, structural assessment, historical designation status. | "The historic warehouse has original windows that must be restored, not replaced." |

Having this information on hand transforms your study from a guessing game into a strategic planning tool.

A project's scope is its constitution. It sets the laws and boundaries for every subsequent decision. Without a well-defined scope, your financial projections are built on a foundation of sand, vulnerable to the slightest pressure.

The Power of a Clear Vision

Think about the difference here. One developer has a vague goal to build "an office building." Another has a sharply defined project: "a 50,000-square-foot, Class A office building targeting tech startups, featuring collaborative open-plan spaces, a rooftop terrace, and LEED Silver certification." The second vision is a real roadmap, giving you everything you need for accurate cost estimates and revenue projections.

This clarity is even more critical for an adaptive reuse project. You're not starting with a blank canvas. If you're turning an old warehouse into loft apartments, you have to meticulously document the building's existing condition—its structural quirks, historical significance, and material limitations. A detailed assessment of the facade, windows, and interior columns will tell you what you can keep and what you have to replace, which has massive financial consequences.

Nailing the scope from the very beginning ensures every dollar in your pro forma is tied to an achievable, real-world plan.

Nailing Down Your Hard and Soft Project Costs

Any credible feasibility study lives or dies by its budget. Your project costs are the biggest variable you'll have to wrestle with, and they fall into two main buckets: hard costs and soft costs. Getting a handle on what goes into each is the first real step toward building a budget that won't crumble under pressure.

Hard costs are all the tangible, physical things you spend money on during construction. Think bricks, steel, drywall, and the labor to put it all together. These are the costs for everything you can literally see and touch, and they make up the lion's share of your construction budget.

Soft costs, on the other hand, are the less obvious—but just as vital—expenses. This category covers everything from your architect’s design fees and engineering plans to the legal paperwork, city permits, and the interest on your construction loan. I've seen more projects get derailed by underestimating these costs than almost any other factor.

Detailing the Hard Costs

To get a grip on hard costs, you have to start with a detailed breakdown of materials and labor. For a new commercial building, that means pricing out foundations, framing, roofing, HVAC systems, and all the interior finishes.

Adaptive reuse projects, like turning an old warehouse into loft apartments, throw a few curveballs. Here, your hard costs have to include things like selective demolition, critical structural repairs, asbestos abatement, and maybe even highly specialized work like restoring historic windows to meet preservation standards.

The best way to get reliable numbers is to bring a general contractor into the loop early. Hand them your preliminary drawings and scope of work to get an initial "cost per square foot" estimate. For instance, a contractor might give you a ballpark of $200 per square foot for a basic office upfit. But that number could easily jump to $275 per square foot or more for a high-end restaurant build-out that requires custom millwork and a full commercial kitchen.

You absolutely have to build in a contingency for things you can't control. A sudden spike in steel prices or a shortage of skilled electricians can blow a hole in the most carefully planned budget. A hard cost contingency of 5-10% isn't just a good idea; it's a non-negotiable part of any responsible financial model.

Unpacking the Often-Overlooked Soft Costs

Soft costs are the silent budget killers. While you can create a pretty straightforward list for hard costs, soft costs are more varied and can add up alarmingly fast. They typically represent 25-30% of total project costs, so getting this part wrong can be a fatal error in your analysis.

Let's pull back the curtain on the usual suspects in this category:

- Professional Fees: This is your A-team—architects, structural and civil engineers, interior designers, and any specialized consultants you might need, like landscape architects or AV experts.

- Permits and Approvals: The fees for building permits, zoning applications, utility tap-ins, and municipal impact fees can be surprisingly high and vary wildly from one city to another.

- Financing and Legal: Don't forget the loan origination fees, interest carry on the construction loan, appraisal costs, and the legal fees for setting up your LLC, reviewing contracts, and closing the deal.

- Insurance: Builder's risk insurance and general liability are significant line items you can't go without.

Think about an adaptive reuse project targeting Historic Tax Credits. Your soft costs will instantly expand to include a historic preservation consultant, fees for the extensive National Park Service documentation, and higher architectural fees to navigate the complex design requirements. If you miss those specialized costs, your feasibility study is fiction.

Many projects look fantastic on paper until the full weight of soft costs is factored in. Diligent tracking of these "invisible" expenses is what separates a successful development from a financial cautionary tale.

Building a Bulletproof Budget

To assemble a truly comprehensive budget, you need a detailed line-item spreadsheet that clearly separates hard and soft costs. Resist the temptation to lump items together. Instead of a single line for "Permits," break it down into "Building Permit Fee," "Zoning Variance Application," and "Sewer Connection Fee." This level of detail forces you to do your homework and find the actual costs instead of just plugging in a guess.

Finally, just like with hard costs, you need a separate contingency for the soft side. A 10% soft cost contingency can be a lifesaver when you run into an unforeseen legal snag or a drawn-out design review process with the city. By meticulously accounting for every expense—both the obvious and the hidden—your financial feasibility study transforms from an academic exercise into a powerful, real-world decision-making tool.

Building a Realistic Pro Forma and Revenue Model

Alright, you've nailed down your costs. Now it's time to bring your project's financial story to life with the pro forma. This is more than just a spreadsheet; it's a dynamic financial model that maps out your development's performance over a 5- to 10-year horizon. This is where your hard-won cost estimates finally meet your revenue projections to show investors if the deal pencils out.

The pro forma is the grand central station for all your data—hard costs, soft costs, financing terms, revenue streams, and operating expenses—all flowing into one powerful narrative. It translates your architectural vision and market research into the language of finance, forecasting potential returns, cash flow, and profitability. I've seen great projects die because of a flimsy pro forma and complex deals get funded on the strength of a well-defended one.

Developing Defensible Operating Assumptions

Before you can even think about revenue, you have to get real about what it's going to cost to run the building once it’s stabilized. These operating expenses are the day-to-day costs that will chip away at your gross income. Underestimate them, and you’re setting yourself up for dangerously optimistic—and frankly, unbelievable—return projections.

Your operating assumptions have to be grounded in reality, not wishful thinking. So, let’s list out every anticipated expense.

- Property Management Fees: Expect to pay 4-10% of effective gross income. This covers the day-to-day grind of managing the property, from chasing down rent to dealing with tenant issues.

- Repairs and Maintenance: This is for the routine stuff—leaky faucets, HVAC servicing, landscaping. A solid rule of thumb is to budget 1-3% of the property's value every year.

- Property Taxes: This is often one of your biggest line items. You can't just guess. You need to dig into local millage rates and assessment practices to get a real number.

- Insurance: Property and liability insurance are absolutely non-negotiable. Get quotes from a commercial insurance broker based on your building's specifics.

- Utilities: In commercial properties with triple-net (NNN) leases, tenants usually cover their own utilities. But for multifamily or gross lease deals, the owner is on the hook. You have to budget for water, sewer, trash, and common area electricity.

Remember to tailor these assumptions to your specific project. An adaptive reuse of a historic building might come with higher maintenance costs for preserving original materials or servicing specialized systems—that has to be in your model. Forgetting to budget for something as simple as annual window washing on a mid-rise can throw your net operating income (NOI) off track.

Projecting Revenue with Market Data

With expenses mapped out, let's shift to the top line: revenue. Your projections must be built on a foundation of current, verifiable market data. This is where you prove that people will actually pay the rents you need to charge.

Start by digging into comparable properties, or "comps," in your specific submarket. For a multifamily project, that means looking at the price per square foot for similar unit types—studios, one-bedrooms, etc. For commercial space, you're analyzing rental rates for similar office, retail, or industrial properties. Don't just look at what landlords are asking for; find out what leases are actually being signed for. There can be a big difference.

Another crucial metric is the absorption rate—the pace at which available units are getting leased up. If you're entering a market with high vacancy and slow absorption, you must model a longer lease-up period. That means more months of carrying costs before the property stabilizes and starts printing money.

Your pro forma is a story you're telling to investors and lenders. Every number, from your assumed rent growth to your vacancy rate, must be a defensible chapter in that story, backed by credible market evidence.

Don't forget to look for secondary income sources. For a residential building, this could be fees for parking, storage units, pet rent, or applications. In a commercial project, you might generate revenue from signage or by leasing rooftop space to a telecom company. These streams might seem small, but they add up and can really polish your overall return profile.

Finally, you have to consider the human element of your target market. For instance, projects in areas with lower financial literacy can face unique hurdles. The IMF's Financial Access Survey shows a clear link between financial literacy and the ability to adopt new financial services. This suggests that in some markets, you might even need to budget for tenant education to ensure long-term stability and on-time payments. To dig deeper into this, you can find insights from the IMF Financial Access Survey. Building a truly realistic model means looking beyond the numbers to the people who will actually live or work in your space.

Securing Financing And Leveraging Incentives

With a solid pro forma in hand, your project stops being just an idea and becomes a real investment opportunity. This is where the rubber meets the road—it’s time to secure the capital to bring your vision to life. Navigating the world of real estate financing can feel like a maze, but your financial feasibility study is the map that will guide you and, more importantly, convince lenders and investors to come along for the ride.

Think of your study as the project's official resume. It’s the first thing a lender will look at to gauge risk and decide if your numbers hold up under scrutiny.

Navigating The Capital Stack

Very few real estate deals get funded by a single check. Instead, you'll build a "capital stack," which is just a fancy way of saying you're layering different types of money from different sources. Imagine it as a pyramid: the most secure money sits at the wide base, and the riskiest—but often most profitable—sits at the peak.

-

Senior Debt: This is your main loan, usually a construction loan from a bank. It’s the biggest piece of the puzzle, typically covering 60-75% of your total project costs. Lenders will tear apart your feasibility study—from your cost estimates to your rent roll—before they sign off on this.

-

Mezzanine Debt: This is a secondary, more expensive loan that bridges the gap between your senior debt and the cash you're putting in. It's riskier for the lender, so it comes with higher interest rates. You might use this if you want to keep more of your own cash out of the deal.

-

Equity: This is the skin in the game. It’s the cash you or your partners contribute. You’re in the riskiest position here, but you also stand to gain the most if the project is a home run. Equity can come from your own pocket, a joint venture (JV) partner, or a pool of private investors.

The way you structure this stack has a massive impact on your bottom line. A project loaded with pricey mezzanine debt needs much stronger revenue to pencil out compared to one funded with a healthier slice of equity.

The Power Of Government Incentives

Beyond the usual bank loans and investor cash, government incentives can completely rewrite your project's financial story. These programs exist to encourage specific kinds of development, like breathing new life into a historic neighborhood or building much-needed affordable housing. For a developer, they can be a total game-changer.

One of the most powerful tools out there, especially for the adaptive reuse projects we're talking about, is the Federal Historic Tax Credit (HTC) program. This isn't a deduction; it's a direct, dollar-for-dollar credit against your federal tax bill, equal to 20% of your qualified rehabilitation expenses.

Don't think of incentives like Historic Tax Credits as just a nice little bonus. On many deals, they are the critical ingredient that makes an otherwise marginal project not just possible, but profitable.

Let's put that into perspective. On a $5 million historic renovation, the HTC could generate a $1 million tax credit. Developers often "sell" these credits to large investors who need to lower their tax liability, generating a huge chunk of upfront cash equity for the project. That infusion of capital can dramatically reduce the amount of debt you need to take on or the amount of cash you have to pull out of your own pocket.

Comparing Common Financing Sources and Incentives

To build a strong capital stack, you need to understand how traditional financing and government incentives can work together. Each plays a distinct role in getting your project funded and across the finish line.

| Type | Primary Function | Example | Impact on Feasibility |

|---|---|---|---|

| Senior Debt | Provides the bulk of the project's capital for construction and stabilization. | Traditional Bank Construction Loan | The foundation of the capital stack; lower interest rates but stricter lending criteria. |

| Mezzanine Debt | Fills the gap between senior debt and equity. | Subordinated Loan from a Private Lender | Increases leverage but adds significant interest costs, requiring stronger returns. |

| Investor Equity | Provides the "at-risk" capital and secures ownership. | Joint Venture (JV) Partnership | Reduces the developer's cash requirement but dilutes ownership and future profits. |

| Historic Tax Credits | Generates cash equity by monetizing a federal tax incentive. | Federal 20% HTC Program | Directly reduces the equity gap, making tough historic preservation deals viable. |

| New Markets Tax Credits | Encourages investment in low-income communities. | NMTC Allocation from a CDE | Provides a significant subsidy, often enabling projects that otherwise wouldn't pencil. |

| TIF / Public Grants | Provides direct public funding for infrastructure or specific project costs. | Tax Increment Financing (TIF) District | Can cover major costs like public improvements or environmental remediation, lowering the overall budget. |

As you can see, these tools aren't mutually exclusive. The most successful projects often weave together multiple sources to create the most resilient and profitable financial structure possible.

Positioning Your Project For Approval

At the end of the day, lenders and investors hate surprises. They are fundamentally risk-averse. They need to see a clear, logical, data-driven story that shows how they will get their money back, plus a return. Your financial feasibility study is what tells that story.

A lender wants to see that you've sweat the details and built a realistic plan. This goes beyond just your numbers. Stable government policy, for example, is a critical but often overlooked factor. The Principal Financial Group's Global Financial Inclusion Index noted that while access to credit is getting better, policy confusion can hinder growth. This highlights just how crucial predictable incentive programs are for a project's financial health. You can read more about these findings in the 2025 research from Principal.

By digging into all the financing options and strategically layering in available incentives, you can build a capital stack that not only makes your project more attractive to funders but also drastically de-risks the entire venture from day one.

Analyzing Risk to Make a Confident Go/No-Go Decision

You’ve built the pro forma, lined up the financing, and the project looks fantastic—on paper. But the real world is rarely as clean as a spreadsheet.

This is where you move from forecasting to stress-testing. The final, critical step in any real-world financial feasibility study is to deliberately try and break your own model. You have to confront the risks head-on to make a confident go/no-go decision.

A static financial model gives you a single snapshot of a possible future. A proper risk analysis turns that snapshot into a full-length movie with multiple potential endings. It prepares you for the inevitable plot twists that come with development, like a sudden market downturn, construction delays, or unexpected cost surges.

Stress-Testing Your Model With Sensitivity Analysis

The first tool you’ll want to grab is sensitivity analysis. The entire process is built around asking one simple question: "What if?" It’s a systematic way to test how sensitive your key financial metrics—like your Internal Rate of Return (IRR) or cash-on-cash return—are to changes in your core assumptions.

Instead of working with just one set of numbers, you create a range of scenarios. Think of it as a base case, a best case, and a worst case. This shows investors you’ve thought through the entire spectrum of possibilities, not just the rosy one.

Here are a few critical variables I always test:

- Construction Costs: What happens to your IRR if hard costs jump by 5%? What about 10%? In today’s world of supply chain issues and labor shortages, this isn’t just a theoretical exercise.

- Lease-Up Velocity: What if it takes six months longer than you planned to reach stabilized occupancy? You need to see how that delay impacts your loan carry and initial cash flow.

- Market Rents: Let’s say rents come in just $1.00 per square foot lower than your projections. At what point does the deal stop making sense? You need to know that number.

- Exit Cap Rate: What if the market softens and your exit cap rate increases by 50 basis points when you plan to sell? This one variable can dramatically impact your final profit.

By plugging these different values into your pro forma, you can see exactly which assumptions pose the greatest threat to your project’s profitability. If a tiny tweak in one variable causes a massive swing in your returns, you've just found a major vulnerability that needs a solid mitigation plan.

Finding Your Tipping Point With Break-Even Analysis

While sensitivity analysis explores a range of outcomes, break-even analysis is all about identifying a single, crucial data point: the absolute minimum performance required for your project to survive.

It answers the gut-check question, "What is the lowest occupancy rate or rental rate we can hit and still pay our bills?"

This isn't about making a profit; it's about staying solvent. You’re calculating the exact point where your total revenues equal your total expenses, including that all-important debt service.

A break-even analysis strips away the optimism from your projections and reveals the project's financial floor. Knowing this number gives you a clear line in the sand—a benchmark you must exceed to keep the lights on.

For a commercial real estate project, we often express this as a break-even occupancy rate. For instance, you might run the numbers and find that you need to be 85% leased just to cover the mortgage, property taxes, insurance, and operating expenses. Anything below that, and you're losing money every single month. That insight is invaluable for setting leasing targets and understanding the real-world pressure of your loan.

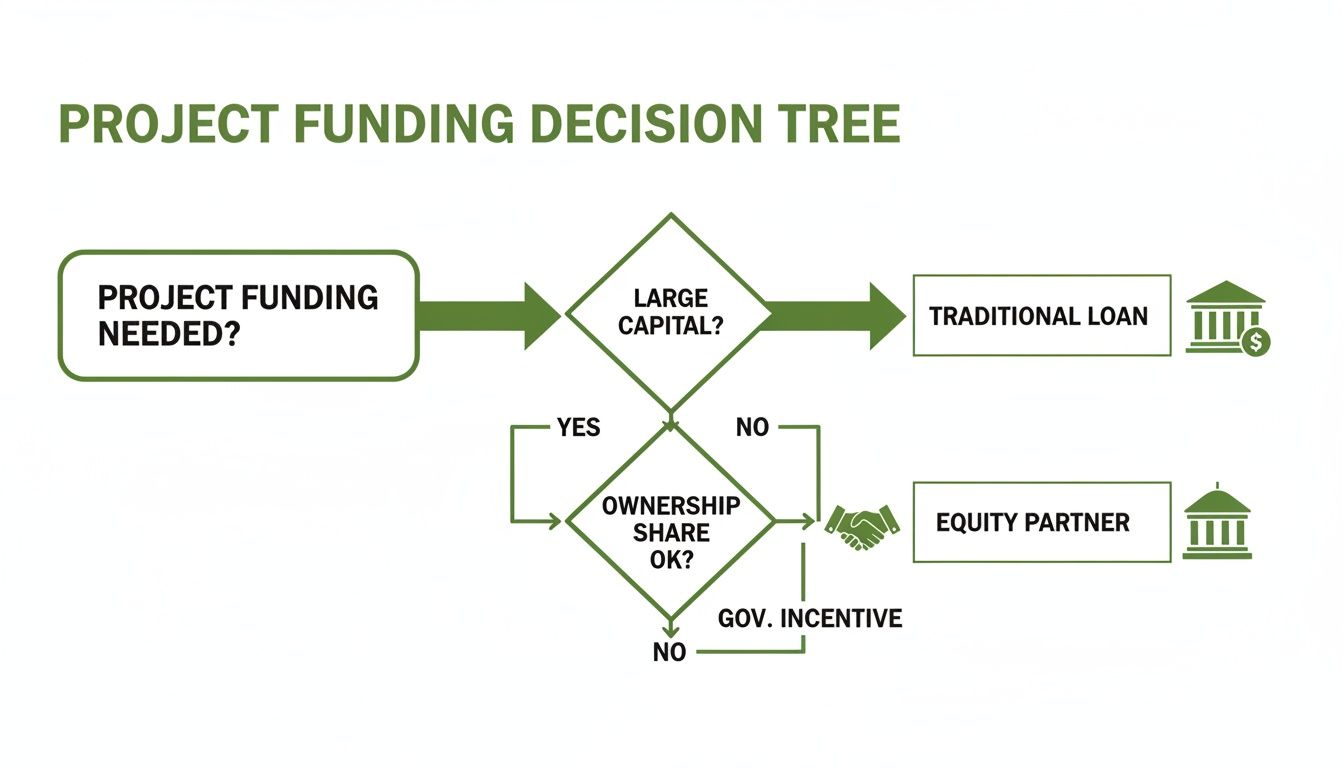

This decision tree gives a high-level view of the funding paths you might consider, each leading to different outcomes for your capital stack and ownership structure.

As the chart shows, a project's needs—from the sheer size of the capital required to how much ownership you're willing to dilute—will point you toward the most logical financing strategy, whether it’s traditional debt, partnerships, or specialized incentives.

Making the Final Call With Decision Criteria

After all the analysis, it’s time to make the call. Your risk assessment gives you the data, but you still need a clear framework to interpret it. The go/no-go decision ultimately boils down to whether the projected returns are worth the risks you're taking on.

Most experienced developers and investors I know rely on three primary metrics to make this final judgment:

- Internal Rate of Return (IRR): This is the annualized rate of return the project is expected to generate. A higher IRR is obviously better, but the key is to compare it against your "hurdle rate"—the minimum acceptable return you've set for a project with this specific risk profile.

- Net Present Value (NPV): NPV calculates the value of all future cash flows (both positive and negative) in today's dollars. It’s simple: if the NPV is positive, the project is expected to generate more value than it costs. That makes it a financially sound decision.

- Cash-on-Cash Return: This is a straightforward metric that measures the annual pre-tax cash flow you receive as a percentage of the total cash you invested. It gives you a clear picture of the return on your actual equity in the deal, which is critical for evaluating performance during the operational phase.

By stress-testing your assumptions and measuring the outcomes against these established criteria, you turn your financial study from a static report into a powerful, dynamic decision-making tool. It's this rigorous process that gives you the clarity and confidence to either walk away from a bad deal or move forward on a great one with your eyes wide open.

Common Questions About Real-World Feasibility Studies

Even with a clear road map, some questions always pop up—from first-time developers and seasoned pros alike. Getting a handle on these common queries helps take the mystery out of the process and really drives home why this upfront work is so critical. Let's dig into some of the most frequent questions I hear.

Feasibility Study vs. Business Plan: What's the Real Difference?

This is a classic, and the distinction is crucial. Think of a financial feasibility study as the investigative work you do before even thinking about breaking ground. Its entire job is to answer one fundamental question: "Does this project actually make financial sense?" It’s all about scrutinizing costs, potential revenue, and all the things that could go wrong to see if an idea is truly viable.

A business plan, on the other hand, comes after you've decided the project is a go. It’s the strategic playbook that answers, "Okay, how are we actually going to pull this off?" It gets into the weeds of operations, marketing, and the financial strategy for bringing the approved project to life.

In short, the feasibility study is the detective asking if a crime was committed; the business plan is the architect drawing up the blueprints for the new building.

What's the Price Tag for a Professional Financial Feasibility Study?

Honestly, it's all over the map and depends entirely on how big and knotty your project is.

- Smaller Projects: If you're looking at a straightforward commercial upfit or a small handful of residential units, you're probably in the $3,000 to $15,000 range.

- Mid-Sized Developments: For something more complex, like a mid-sized mixed-use building, the cost can climb to anywhere from $15,000 to $50,000.

- Large-Scale Projects: When you get into massive, intricate developments with layered financing, multiple phases, or major public incentives, the cost can easily blow past $50,000.

It's tempting to see this as just another expense, but that's the wrong way to look at it. This is an investment. Spending this cash upfront can save you from a catastrophic financial loss on a project that was doomed from the start.

What Are the Biggest Mistakes People Make?

I see the same missteps time and again. The number one mistake, without a doubt, is overly optimistic revenue projections. People fall in love with their idea and assume rents or sales prices that just aren't supported by hard market data. Right behind that is underestimating soft costs—that’s a classic budget-killer.

The most dangerous trap is confirmation bias. It's human nature to look for data that confirms what you want to be true, instead of objectively assessing what is true. You have to constantly challenge your own assumptions and put your numbers through the wringer.

Using old market research or, even worse, skipping a thorough sensitivity analysis are also huge red flags. If your study doesn't include a believable "worst-case" scenario, it’s not finished. For a wider view, you can check out a comprehensive guide on conducting feasibility studies that also dives into market demand and technical issues.

Can I Just Use a Template for My Study?

Templates can be a great place to start. They give you a framework for organizing your costs, revenue, and key metrics, which helps make sure you don't forget a major category.

But let me be clear: a template is not a substitute for project-specific research and analysis. Every single real estate deal is a unique puzzle of site conditions, local market quirks, zoning laws, and construction variables. A generic spreadsheet can't capture any of that nuance.

So, use a template as your guide for structure, but make sure every single number you plug into it is customized, researched, and rigorously tested for your project. Your final report needs to be a bespoke document, not a fill-in-the-blanks homework assignment.

At Sherer Architects, LLC, we guide developers and investors through these critical questions every day. Our deep experience in commercial, adaptive reuse, and historic preservation projects means your financial study is built on decades of real-world design and construction knowledge. Let us help you build a solid foundation for your next project.