At its core, a financial feasibility study answers the most important question you can ask before breaking ground: Will this project actually make money? It's a hard-nosed, data-driven look at a proposed venture's viability, weighing everything from the initial cash outlay and projected income to potential risks and the ultimate return on investment.

This analysis is the critical go/no-go signal for any serious developer or investor.

Your Blueprint for a Profitable Real Estate Venture

Long before we sketch the first line or a single shovel hits the dirt, a financial feasibility study acts as the project's strategic roadmap. It's about moving past a gut feeling and transforming a promising idea into a bankable business case supported by cold, hard numbers.

For complex undertakings like commercial real estate development and especially adaptive reuse, this analysis isn't just a preliminary step—it's the bedrock for every decision that follows. It forces you to pressure-test your assumptions against market realities, ensuring the architectural vision is firmly tethered to financial practicality.

Think of it as the business plan for the building itself. A well-executed study becomes your most powerful tool for securing financing, as it proves to lenders and investors that you’ve done your homework and have a clear-eyed view of the path to profitability.

What We Aim to Achieve

The main objective is to determine if a project makes economic sense before anyone commits serious capital. This means digging deep into several key areas:

- Validating the Concept: Does the market demand and projected revenue justify the development costs? Simple as that.

- Spotting Financial Risks: The study is designed to uncover hidden vulnerabilities—things like potential construction overruns, a slower-than-expected lease-up, or a sudden shift in interest rates.

- Fine-Tuning the Project Plan: Often, the findings reveal opportunities to tweak the project's scope, scale, or even the design to get a better financial result.

- Building Investor Confidence: Nothing speaks louder to capital partners and lenders than a transparent report filled with data-backed evidence.

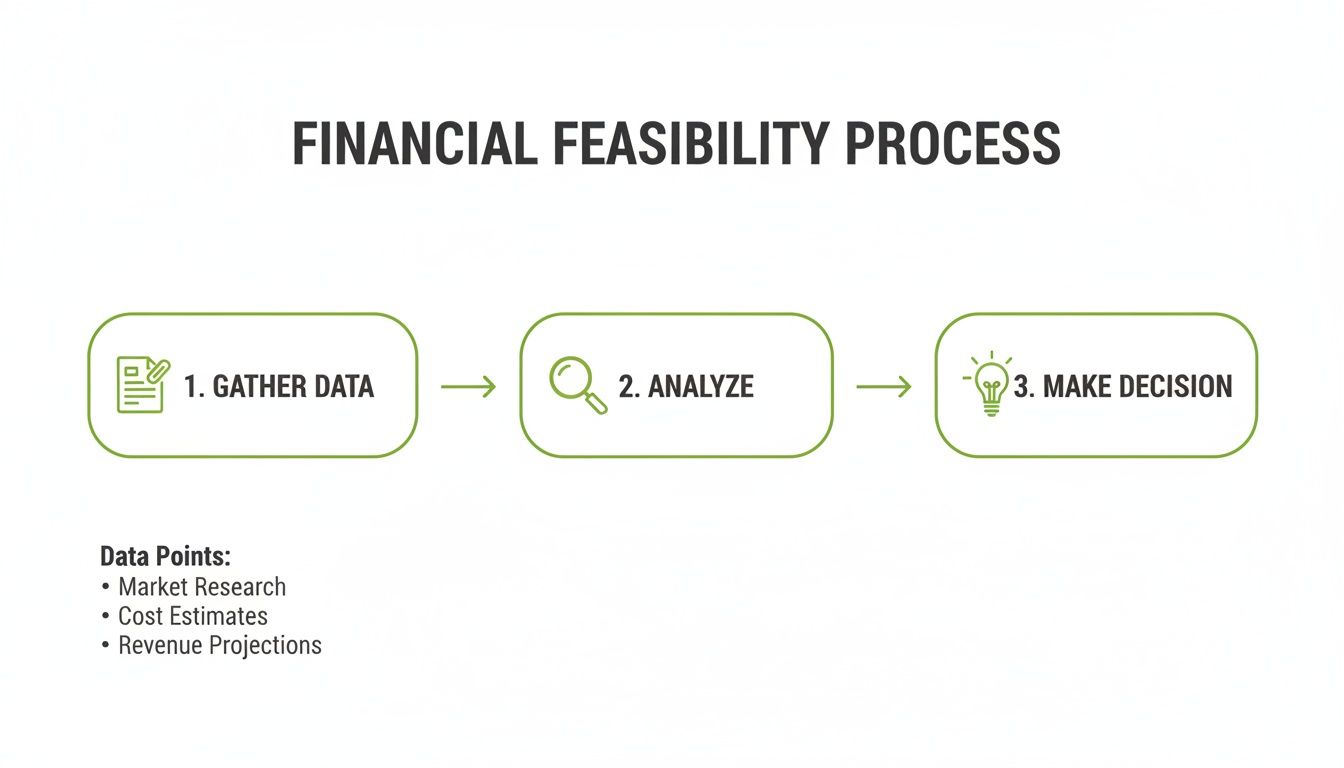

The whole process is about simplifying complex financial decisions by breaking them down into a clear, logical workflow.

As you can see, every solid study follows this progression. We gather the right data, run the numbers, and empower you to make a smart, informed decision.

A well-structured study pulls together several critical pieces of analysis. This table gives a snapshot of the core components we always include to build a complete financial picture.

Key Components of a Financial Feasibility Study

| Component | Objective | Key Metric Examples |

|---|---|---|

| Market Analysis | Assess demand, competition, and rental/sale price potential. | Vacancy Rates, Absorption Rates, Comparable Rents/Sales |

| Cost Estimation | Project all hard and soft costs from acquisition to stabilization. | Cost per Square Foot, Contingency Budgets (e.g., 10-15%) |

| Revenue Forecasting | Model potential income streams over the project's lifecycle. | Gross Potential Rent, Vacancy Loss, Effective Gross Income |

| Financing Structure | Determine sources and uses of funds, including debt and equity. | Loan-to-Value (LTV) Ratio, Debt Service Coverage Ratio (DSCR) |

| Profitability Analysis | Calculate the expected return on investment. | Cash-on-Cash Return, Internal Rate of Return (IRR), ROI |

| Sensitivity Analysis | Stress-test the pro forma against potential market shifts. | Best/Worst/Base Case Scenarios for Rent, Costs, and Vacancy |

Each of these components informs the others, creating a dynamic financial model that accurately reflects the project's potential.

Why It's Non-Negotiable for Adaptive Reuse

For adaptive reuse projects, particularly those involving historic buildings, the financial feasibility study becomes even more crucial. These ventures come with a unique set of challenges and opportunities that you just don't see in new construction.

A study for an adaptive reuse project has to meticulously account for variables like historic tax credits, the cost of unforeseen structural repairs, and the potential for premium rents that come with a building's unique character. Getting this wrong leads to flawed projections and serious financial exposure.

For example, turning an old warehouse into loft apartments involves far more than standard construction estimates. We have to factor in the real costs of things like hazardous material abatement, navigating the demands of preservation boards, and sourcing specialized labor.

But on the flip side, we can model the enormous financial upside of state and federal historic tax credits, which can completely change a project’s capital stack and supercharge its ROI.

In the end, this study isn't just another box to check. It’s a powerful risk-mitigation tool that protects your investment, gets all your stakeholders on the same page, and sets the stage for a project that isn't just an architectural landmark, but a genuine financial success.

Building an Accurate Project Cost Estimate

A financial feasibility study lives and dies by the quality of its cost projections. If you lowball the budget, you're setting yourself up for a cash flow crisis down the road. But if you pad the numbers too much, you might walk away from a project that could have been a real winner.

The key to a realistic budget is a meticulous breakdown of every single expense, separating the physical construction from all the other essential costs. It all starts with two fundamental categories: hard costs and soft costs. Nail these, and you’ll have a pro forma that can withstand scrutiny from lenders, investors, and even your own team.

Decoding Hard Costs

Hard costs are the most tangible part of your budget—they’re what most people think of when they imagine construction. We're talking about the bricks, mortar, steel, and labor that bring architectural plans to life. If you can physically touch it or watch it being installed on-site, it’s a hard cost.

To get your arms around these numbers, you need to be grounded in current market data. Keeping an eye on regional benchmarks, like the latest UK building costs per square metre, can give you a solid starting point for back-of-the-envelope calculations, no matter where your project is located.

A typical hard cost breakdown will always include:

- Site Work: All the prep work before you can go vertical, including demolition, excavation, grading, and running utilities.

- Foundation and Structure: The building's skeleton—concrete, steel beams, framing, and the roof.

- Exterior Finishes: Everything that makes up the building's skin, like siding, masonry, windows, and doors.

- Interior Finishes: Drywall, flooring, paint, cabinetry, light fixtures, and all the details that make a space usable.

- MEP Systems: A huge line item covering all mechanical, electrical, and plumbing work.

- Landscaping and Paving: The final touches, from sidewalks and parking lots to green spaces.

While these are often estimated on a per-square-foot basis initially, a truly reliable estimate only comes from getting detailed quotes from general contractors and subs who know the local labor and materials market inside and out.

In our experience, the biggest budget surprises often come from what’s hidden. For adaptive reuse projects, this could be anything from asbestos that needs abatement to a foundation that requires unexpected reinforcement. A thorough pre-construction assessment is non-negotiable.

Accounting for Soft Costs

While hard costs are about the physical build, soft costs cover all the essential—yet less tangible—expenses needed to design, permit, and manage the project. It's a common mistake to overlook these in early estimates, but they can easily swallow 25-30% of your total project budget. Ignoring them is a recipe for disaster.

Think of soft costs as the professional services and administrative fees that make the whole thing possible. They are just as vital to your financial study as the price of concrete.

Make sure you've budgeted for these key soft costs:

- Architectural and Engineering Fees: The price for the design, blueprints, and structural engineering expertise.

- Permits and Inspection Fees: The non-negotiable municipal charges for building permits, zoning applications, and site inspections.

- Legal and Accounting Fees: Costs tied to property acquisition, reviewing contracts, and financial oversight.

- Financing Costs: Fees from your lender, like loan origination, appraisals, and the interest you'll pay during construction.

- Insurance: Builder’s risk, liability, and other policies needed to protect the project during construction.

- Real Estate Commissions: Broker fees for acquiring the land or property.

Budgeting for the Unpredictable

No project ever goes exactly as planned. This is especially true for adaptive reuse and historic preservation. That’s why a contingency fund isn't a "nice to have"—it's a critical line item in any credible budget. This isn’t a slush fund; it's a calculated reserve set aside for unforeseen problems, scope changes, or sudden material price spikes.

For brand-new construction, a contingency of 5-10% of hard costs is a safe bet. But for complex adaptive reuse projects where you’re almost guaranteed to uncover surprises, we strongly recommend a contingency of 15-20%, sometimes even more.

This buffer is what protects your project from delays and financial strain, giving you the capital to handle surprises without derailing the entire venture. A healthy contingency is what turns a hopeful guess into a resilient financial plan.

Forecasting Revenue to Project Long-Term Profitability

Once you've nailed down your project costs, you have to pivot to the other side of the ledger: income. A building's success isn't just about controlling what you spend; it's about what it can earn. This is where we shift from construction budgets to the art and science of revenue forecasting, which truly forms the heart of your pro forma.

A believable revenue model isn't just wishful thinking. It's a detailed, multi-year projection built on hard market data, a clear-eyed look at the competition, and a solid grasp of what makes your property special. This process is how you turn an architectural vision into a financial story that makes lenders and investors feel secure.

Grounding Your Projections in Market Reality

Any credible forecast starts with a deep dive into the local market. You have to anchor every assumption in what's happening on the ground, right now. This means getting granular—forget city-wide trends and focus on your specific neighborhood and property type.

The first number to establish is your Gross Potential Rent (GPR). Think of this as the absolute best-case scenario: the total income you’d collect if every square foot was leased 100% of the time at full market rates. To get this number right, you need to run a thorough competitive analysis, or "comp study."

Here’s what that looks like in practice:

- Find Your Rivals: Pinpoint at least 3-5 similar properties right in your area. You’re looking for buildings of a similar age, class (A, B, or C), and size, with amenities that match what you're offering.

- Analyze Real Rents: What are they actually charging per square foot? Don't get distracted by the asking price on a website; find out what tenants are truly paying.

- Check Vacancy Rates: If the building next door is half-empty, that’s a huge red flag. It points to weak demand or too much supply. On the flip side, if everything is leased up, you're in a healthy market.

This legwork gives you the hard data you need to set a realistic market rent for your own units, creating the baseline for your entire income model.

When it comes to adaptive reuse, a standard comp study might not capture the full picture. The unique character of a historic building—think exposed brick, soaring ceilings, or original hardwood—can often demand a premium. We’ve seen tenants gladly pay 10-15% more for a space with authentic soul compared to a new, cookie-cutter box.

From Gross Potential to Realistic Income

Let's be honest: no building is ever 100% full all the time. To get from a theoretical maximum to a real-world projection, you have to factor in vacancies and potential credit loss. This calculation gives you the Effective Gross Income (EGI), a much truer picture of the cash you'll actually collect.

Your EGI is simply your GPR minus a vacancy allowance. In a strong market with a stabilized property, assuming a 5-7% vacancy rate is a safe bet. But if you’re launching a new development, you have to be more realistic. For the initial lease-up period, you might model a much higher vacancy that slowly shrinks over the first 12-24 months.

And don't overlook other income streams, often called ancillary income. This is money that comes from sources other than rent checks.

This could include things like:

- Parking fees

- Renting out storage units

- Coin-operated laundry

- Vending machines

- Common Area Maintenance (CAM) charges passed through to tenants

These might seem small, but together they can make a real difference to your bottom line.

Calculating Key Profitability Metrics

With your income and expenses mapped out, you can finally calculate the core metrics every investor is waiting for. These numbers are the bottom line; they distill your entire pro forma into a few powerful figures that signal whether the project is a winner.

These are the three most critical metrics you'll need:

Net Operating Income (NOI): This is the pure profit your property generates before you pay the mortgage or taxes. It's the cleanest measure of performance, calculated as: EGI – Operating Expenses = NOI. This is the single most important number in real estate investment.

Capitalization Rate (Cap Rate): This metric connects the NOI to the property's value, giving you a snapshot of its potential return. The formula is: NOI / Property Value = Cap Rate. A higher cap rate often signals a higher return (but can also mean higher risk).

Cash-on-Cash Return: This gets personal. It answers the investor's main question: "For every dollar I put in, what do I get back each year?" It's calculated as: (NOI – Debt Service) / Total Cash Invested = Cash-on-Cash Return.

By carefully building your revenue forecast from the ground up and translating it into these essential metrics, your financial feasibility study moves beyond theory. It becomes a clear, defensible roadmap to profitability that makes your project an irresistible opportunity.

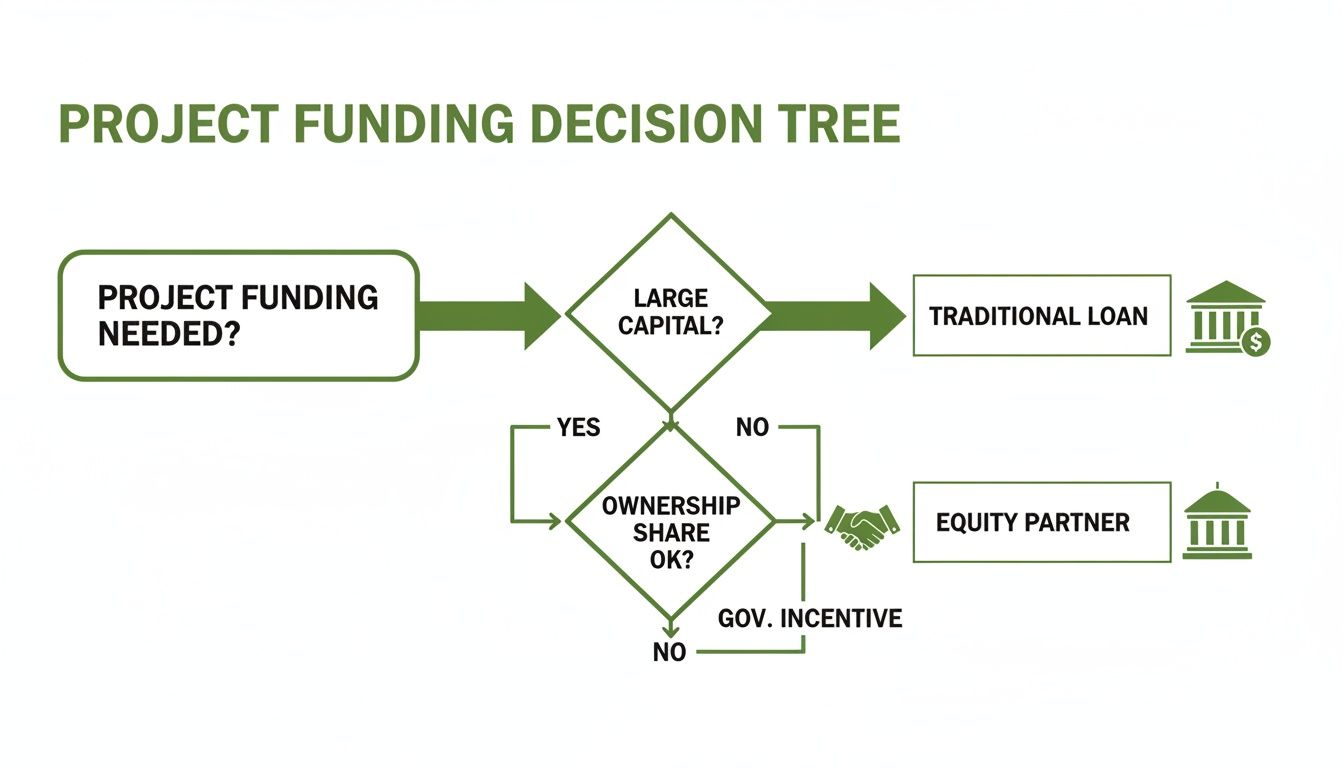

Structuring Your Capital Stack and Securing Financing

You’ve done the hard work. Costs are tallied, revenues are projected, and your financial feasibility study has laid out a clear business case for the project. Now comes the moment of truth: turning all that data into actual capital.

This is where the rubber meets the road. Your study is no longer just a planning document; it’s the single most important tool you have for building confidence with lenders and investors. A well-built capital stack isn't just about getting a loan. It's about strategically blending different funding sources to fit your project’s specific goals, especially for something as complex as adaptive reuse.

The "capital stack" is simply how a project is paid for, layer by layer. Picture it like a pyramid. The most secure, lowest-cost debt sits at the bottom, and the riskiest, highest-return equity lives at the top. Finding the right mix is a balancing act between managing risk and maximizing your potential return. When a lender asks to "see the numbers," your feasibility study is the only answer that matters.

Understanding the Layers of Capital

The foundation for most deals is senior debt, which is usually a commercial mortgage from a bank. It’s the biggest and cheapest piece of the financing puzzle because it’s the safest for the lender—if things go south, they get paid back first. The quality of your feasibility study has a direct impact on the terms you get here. Strong NOI projections and reasonable cost estimates can help you land a higher loan-to-value (LTV) ratio and a more favorable interest rate.

What if senior debt doesn't cover everything? That’s where you might see mezzanine debt or preferred equity. These are more expensive, higher-risk options that bridge the gap between your primary loan and your own cash. Let’s say the bank will only finance 70% of your project. Mezzanine financing could potentially cover another 10-15%. These lenders take on more risk, so they expect a higher return, but they are often the key to getting a deal across the finish line.

At the very top of the pyramid is common equity. This is your skin in the game—the cash you and your partners invest. It’s the riskiest position, but it also gets the biggest rewards when a project succeeds.

Your financial feasibility study is not just an internal document; it's a marketing tool for capital. It proves you've thought through the risks, validated your assumptions, and have a clear, data-driven plan to repay debt and deliver returns.

Specialized Financing for Adaptive Reuse and Preservation

When you’re working on adaptive reuse or historic preservation projects, the capital stack can get far more creative—and much more profitable. These projects often qualify for powerful incentives that can completely change the financial equation. Walking away from these opportunities is like leaving money on the table.

Here are a few programs we see making a huge impact:

- Federal Historic Tax Credits: This is a true game-changer. The federal program offers a tax credit for 20% of qualified rehabilitation costs. For a $10 million renovation, that's a $2 million direct, dollar-for-dollar reduction in your tax bill. Better yet, these credits can often be sold to investors to generate upfront equity.

- State Historic Tax Credits: Many states, including South Carolina, have their own historic tax credit programs. These can be "stacked" on top of the federal credit, shrinking the amount of cash you need to bring to the table even further.

- Preservation Grants and Easements: Don’t overlook grants from local and national organizations dedicated to preserving historic properties. You can also explore placing a facade easement on a building, which can generate a significant tax deduction.

Navigating the complex application process for these programs takes real expertise. An experienced architect can guide you through the compliance maze, making sure your design qualifies while maximizing the financial benefit. What looks like an administrative headache can actually become a cornerstone of your financing strategy.

The entire industry is moving in this direction. Recent AIA data shows that reconstruction projects now make up 62% of revenue from commercial and industrial facilities. That’s a massive jump from just 38% fifteen years ago, highlighting the clear economic momentum behind adaptive reuse.

In the end, assembling your capital stack is all about telling a convincing story. Your financial feasibility study is the script, filled with credible data that shows capital partners your vision isn't just a beautiful design, but a sound, profitable investment.

How to Stress-Test Your Financial Model

So, you’ve built your pro forma. Every cost is itemized and every revenue stream is meticulously projected. But what happens when the real world throws a curveball at your perfect spreadsheet? A truly solid financial feasibility study doesn't just paint a pretty picture; it prepares for a storm.

This is where stress-testing your numbers comes into play. By running a sensitivity and scenario analysis, you can see just how much pressure your project can handle before it breaks. It's how you shift from a static prediction to a dynamic tool that reveals your deal’s true resilience and shows lenders you’ve done your homework.

Identifying Your Project’s Key Variables

First things first, you need to pinpoint the handful of assumptions that really move the needle on your bottom line. These are the variables where a tiny shift can create a massive ripple effect across your returns. For any real estate deal, a few usual suspects always make the list.

The goal is to isolate the numbers that truly drive the financial outcome. To do this right, you first need a solid foundation in building winning real estate financial models that can accurately reflect different outcomes and risks.

Look for variables like these:

- Construction Costs: What happens if material prices jump 10% because of a supply chain snag?

- Interest Rates: How does a 1% or 2% hike in your construction loan rate eat into your profits and impact debt service?

- Lease-Up Period: What if it takes 18 months to hit stabilization instead of your planned 12?

- Market Rents: How would a 5% dip in achievable rents hit your Net Operating Income (NOI)?

- Exit Cap Rate: What if the market cools off and your exit cap rate ticks up by 50 basis points, knocking down your final sale price?

You don't need to test every single line item. Just focus on the big ones—the levers with enough power to fundamentally change your project's financial story.

Running a Sensitivity Analysis

Once you’ve identified your key variables, it's time for a sensitivity analysis. This is where you tweak one variable at a time, keeping everything else the same, to see how it affects your most important metrics, like your Cash-on-Cash Return or Internal Rate of Return (IRR).

You can set this up easily in a spreadsheet with a data table. For instance, put a range of potential construction costs on one axis (e.g., -10%, -5%, Base Case, +5%, +10%) and your IRR on the other. The table will instantly show you just how sensitive your returns are to budget overruns.

This simple exercise is incredibly powerful. You might discover your project can absorb a 10% cost increase without much trouble, but that a slight delay in leasing is absolutely devastating. That kind of insight tells you exactly where to focus your energy on mitigating risk.

It helps you find the true "load-bearing walls" in your financial structure.

Building Out Scenarios

While sensitivity analysis looks at risks one-by-one, scenario analysis bundles them together to tell a more complete story about what the future might look like. Instead of just changing single numbers, you create entire narratives for different potential outcomes.

The common practice is to build out three distinct scenarios to really understand the full spectrum of possibilities.

- Best-Case Scenario: This is your blue-sky, everything-goes-right outlook. Construction finishes early, you lease up faster than planned, rents are higher than you projected, and financing stays cheap. This is your project’s maximum potential upside.

- Most-Likely Scenario: This is your base case—the realistic, grounded projection you’ve already built. It's what you actually expect to happen based on today's market data and reasonable assumptions.

- Worst-Case Scenario: Here's where you model a perfect storm. Costs balloon, the economy dips, leasing grinds to a halt, and interest rates spike. The point isn't to be a pessimist; it's to find out if your project can actually survive a serious downturn. Can it still make its debt payments even under intense pressure?

By modeling these different futures, you get a much deeper understanding of your project’s risk profile. Your financial feasibility study transforms from a simple forecast into a strategic roadmap, letting you make decisions with your eyes wide open to what could be coming.

Answering Your Key Questions About Financial Feasibility Studies

Even with a roadmap in hand, it’s natural to have questions when you’re getting started. Over the years, we’ve found that most developers, investors, and property owners circle back to the same core concerns. Let's tackle some of the most common questions we hear, clearing up the practical details so you can move forward with confidence.

How Much Does a Feasibility Study Cost?

This is usually the first thing people ask, and the honest answer is, it really depends. The price tag is directly tied to how complex and large your project is. A quick look at a small commercial upfit will be a modest expense, but a deep-dive analysis for a massive adaptive reuse project with historic tax credits is a much bigger undertaking.

But here’s how we encourage our clients to think about it: this isn't a cost, it's an investment in de-risking your entire project. A solid, upfront study can save you from sinking millions into a deal that was flawed from the start.

The cost of a good feasibility study is a tiny fraction of the potential loss from a bad investment. It's the cheapest insurance policy you can buy for a multi-million dollar venture.

Ultimately, the fee for a detailed study will be a reflection of the overall project budget. It’s a specialized service that pulls together market research, complex financial modeling, and architectural expertise, and the price reflects that high-level insight.

When Is the Right Time to Perform a Study?

As early as humanly possible. The best time to dig in is often before you even have a property under contract. What you learn can be a powerful tool for negotiating the purchase price and shaping the terms of the deal. The sweet spot is when you have a solid concept but before you’ve committed any serious, non-refundable money.

Here are the key moments in a project's life when a study makes the most sense:

- Before Buying the Property: A preliminary study can validate your offer, making sure the numbers work from day one.

- During Your Due Diligence Period: This is the perfect window for a more detailed analysis. You can uncover any red flags before the deal is final.

- Before You Go Out for Financing: A complete, professional study isn't just a document—it's the foundation of your pitch to lenders and investors.

If you wait until after you’ve hired the full design team or closed on the property, you're too late. The study is meant to guide these big decisions, not just rubber-stamp them after the fact.

How Does It Differ for New Builds vs. Adaptive Reuse?

The basic formula—costs versus revenue—is the same, but that's where the similarities end. The focus and complexity of a study shift dramatically when you're comparing a new build to an adaptive reuse project. Frankly, a new construction study is often more straightforward. The costs are more predictable, and you’re dealing with fewer unknowns.

With adaptive reuse, especially when you’re talking about historic buildings, the analysis gets a lot more interesting.

| Factor | New Construction | Adaptive Reuse |

|---|---|---|

| Cost Estimation | Based on current material/labor rates; fewer surprises. | Must account for unforeseen conditions, abatement, and specialized labor. |

| Revenue Projections | Based on market comps for new, modern spaces. | Can often command premium rents due to unique character and history. |

| Financing Sources | Primarily traditional debt and equity. | Can tap into powerful tools like historic tax credits and preservation grants. |

| Risk Profile | Risks are typically market-driven (e.g., lease-up pace). | Risks include both market factors and hidden construction challenges. |

A feasibility study for an adaptive reuse project requires a much deeper bench of experience. You have to be able to accurately model not just the unique construction risks but also the significant financial incentives that can make these projects so rewarding. It’s a trickier puzzle, but the payoff is often much greater.

Navigating the complexities of a financial feasibility study, especially for adaptive reuse and historic preservation, is our specialty. At Sherer Architects, LLC, we combine rigorous financial analysis with decades of design experience to ensure your vision is both beautiful and profitable. Contact us today to discuss your next project.