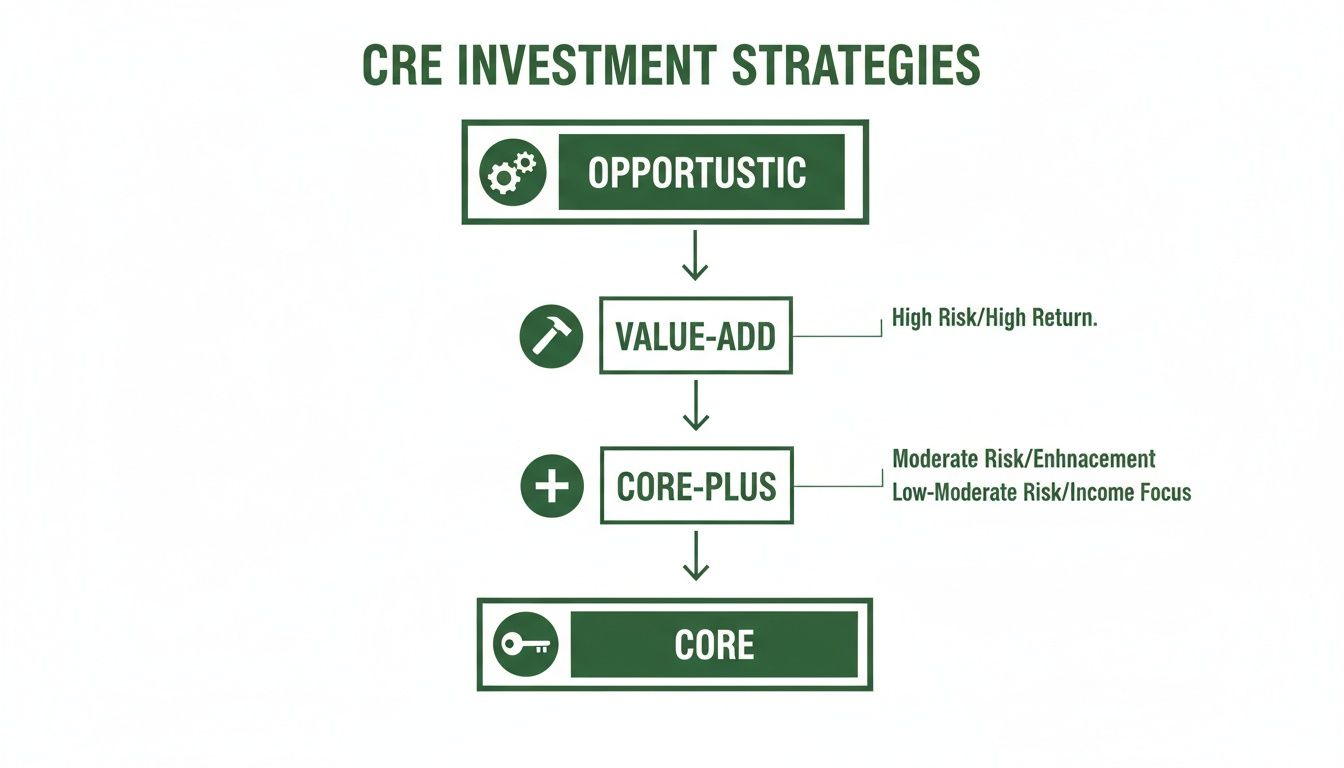

When it comes to commercial real estate, there's no single "right" way to invest. It's really a spectrum, a sliding scale where you balance the risk you're willing to take with the reward you hope to achieve. The industry generally breaks this down into four main approaches: Core, Core-Plus, Value-Add, and Opportunistic.

Getting a handle on this framework is your first real step toward matching your capital with a strategy that actually fits your financial goals.

Understanding The Four Core Investment Strategies

Diving into commercial real estate can feel like you're learning a whole new language, but the entire investment landscape really rests on these four pillars. Each of these strategies simply represents a different appetite for risk and, in turn, a different potential for returns.

Let's make this simple with an analogy I like to use: owning a car. Each strategy is like a different kind of car ownership, from buying a brand-new, reliable daily driver to taking on a high-stakes classic car restoration. This comparison makes it much clearer what you're getting into with each approach.

The Core Strategy: A Dependable Daily Driver

A Core investment is the most conservative play you can make. Think of it as buying a new, top-of-the-line sedan right off the lot. It’s a high-quality, fully functional asset that needs little more than regular oil changes and a car wash.

Properties in this category are usually:

- Located in prime, stable markets with strong fundamentals.

- Fully leased to creditworthy, long-term tenants (think national brands or government agencies).

- Generating consistent, predictable cash flow from the day you close the deal.

The goal here isn't to hit a home run with appreciation. It's about generating stable, low-risk income, much like enjoying a smooth, predictable commute without any surprise breakdowns. The returns are modest but incredibly reliable, which is why this is a favorite for big players like pension funds and insurance companies.

The Core-Plus Strategy: Minor Upgrades for Better Performance

Moving just a bit further up the risk ladder, we land on Core-Plus. This is like buying a well-maintained, three-year-old car. It runs great, but you know a few minor upgrades—maybe some new tires, a modern infotainment system, or a deep interior detailing—could boost its value and performance.

Core-Plus properties are still high-quality, but they have some clear, manageable upside. This might mean making light renovations to common areas, leasing up a few small vacancies, or bumping up below-market rents as leases turn over. As an investor, you’re taking on a little more risk for a shot at slightly higher returns than a pure Core deal.

The Value-Add Strategy: The Major Overhaul

This is where the real hands-on work begins. A Value-Add strategy is like buying a solid but dated car that needs a new engine and a fresh paint job. The vehicle has good "bones," but it’s going to take a significant injection of cash and effort to bring it up to its full potential.

Value-Add properties typically have real problems to solve. We're talking high vacancy rates, years of deferred maintenance, or a need for a complete repositioning to compete in the current market. This approach carries moderate to high risk, but it also offers the potential for a huge payoff in appreciation once you've stabilized the property and executed your business plan.

As this flowchart shows, as you move from Core toward Opportunistic, both the work involved and the potential returns ramp up significantly.

The Opportunistic Strategy: The Frame-Up Restoration

At the very top of the risk-reward pyramid sits the Opportunistic strategy. This is the most aggressive approach, easily compared to a full, frame-up restoration of a rare classic car. You might literally be starting with just a rusted-out frame, which in real estate terms means ground-up development, a massive redevelopment of an obsolete building, or navigating a jungle of complex entitlement and zoning issues.

Opportunistic investing is all about creating value where very little exists today. It demands a ton of capital, deep expertise, and a long-term vision, targeting the highest possible returns to compensate for the immense risk involved.

Comparing CRE Investment Strategy Risk and Return Profiles

To give you a quick at-a-glance reference, here’s how the four strategies stack up against one another. This table breaks down what you can generally expect in terms of risk, returns, and the type of property you’ll be dealing with.

| Strategy | Risk Level | Target IRR (%) | Typical Property Condition |

|---|---|---|---|

| Core | Low | 7% – 10% | Stabilized, fully leased, prime location, Class A |

| Core-Plus | Low to Moderate | 9% – 12% | Mostly stable with minor leasing or cosmetic upgrade potential |

| Value-Add | Moderate to High | 12% – 18% | Significant vacancy, deferred maintenance, needs repositioning |

| Opportunistic | High | 18%+ | Ground-up development, major redevelopment, raw land |

Remember, these are just general guidelines. The exact numbers can shift based on the market cycle, property type, and the specifics of any given deal. Still, this gives you a solid framework for understanding where a potential investment fits on the risk-reward spectrum.

How Market Dynamics Shape Your Investment Approach

Knowing the core strategies is just the starting line. The real art is knowing when to use them. A brilliant value-add plan can get wiped out in a down market, while even a simple core investment can look like a genius move during an economic upswing. The best investors I know don't operate in a bubble; they align every move with the broader economic currents and market sentiment.

I like to think of the market as the weather and your strategy as your vehicle. You wouldn't take a classic convertible out for a spin in a blizzard, right? In the same way, you wouldn’t launch an aggressive ground-up development when financing has dried up and tenant demand is weak. Reading the economic forecast lets you pick the right vehicle—and the right route—for the road ahead.

This is all about turning abstract economic data into on-the-ground intelligence. Are interest rates finally leveling off? Is capital getting easier to find? Are specific cities or property types showing unexpected strength? Answering these questions helps you pivot, adapt, and put your money where it will have the biggest impact.

Riding The Waves Of Investor Confidence

One of the biggest factors at play right now is a major comeback in investor confidence. After a few years of sitting on the sidelines, people are feeling better. Stabilizing interest rates and more realistic asset prices have opened a window of opportunity, and savvy investors are climbing through it.

This isn't just a gut feeling; the numbers back it up. In 2025, global commercial real estate investment volumes bounced back hard, hitting US$213 billion in the third quarter alone. That's a 17% jump from the previous year, with the year-to-date total up 21% over 2024. This wave of capital shows that confidence is returning, especially in the Americas, where activity shot up 26% in Q3, led by the U.S. You can discover more insights about global investment trends and see what they signal for the market.

This kind of capital flow creates its own momentum. When deals get done and people make money, it pulls hesitant investors off the fence, which injects more cash into the market and helps support asset values. For developers and owners, the message is clear: get your projects ready and start deploying capital.

Following The Capital To Hot Sectors

Of course, not all real estate is created equal. Market dynamics always favor certain asset classes, and right now, the money is flowing toward sectors with undeniable, long-term demand. Figuring out why these sectors are so popular is the key to aligning your own commercial real estate investment strategies.

Two clear winners have pulled away from the pack:

- Multifamily: Thanks to a chronic housing shortage and a cultural shift toward renting, apartment buildings are still a go-to for investors. There’s a built-in stability that comes from the constant need for housing, making multifamily a prime target for Core, Core-Plus, and certain Value-Add strategies.

- Industrial & Logistics: The e-commerce boom just keeps going, and the push for more robust supply chains has lit a fire under the industrial sector. Warehouses, distribution hubs, and last-mile facilities are in high demand, making this a hotbed for new development (Opportunistic) and for buying and upgrading older buildings (Value-Add).

The key takeaway here is to hitch your wagon to sectors with a compelling, long-term story. Chasing fads is a good way to lose money, but positioning yourself within a trend driven by fundamental economic shifts dramatically improves your odds.

While multifamily and industrial are grabbing the headlines, that doesn't mean there aren't opportunities elsewhere. The office market, for example, is full of unique adaptive reuse projects where underused buildings are being transformed into exciting mixed-use properties. The secret is matching your own risk appetite and expertise to the specific needs—and potential—of each sector in today's climate.

Unlocking Hidden Value With Adaptive Reuse

While core and value-add strategies work within a building's existing purpose, some of the most exciting returns come from seeing a property not for what it is, but for what it could be. This is the world of adaptive reuse—a strategy that breathes new life into obsolete buildings, turning forgotten properties into high-demand, profitable assets.

It’s all about rewriting a building’s story.

Imagine an old, forgotten textile mill with gorgeous brickwork and soaring ceilings. Through adaptive reuse, it becomes sought-after loft-style apartments. Or that vacant downtown department store? It could be transformed into a sleek, modern tech hub with bustling retail on the ground floor. You're not just renovating; you're giving the structure a completely new economic purpose.

This approach revitalizes communities and often delivers returns that blow more conventional investments out of the water.

The Financial Case For Transformation

Repurposing an old building might sound complicated, maybe even more so than starting from scratch. But for savvy developers, the financial and strategic upsides are often too good to ignore. The benefits go way beyond just saving a piece of local history.

The most obvious advantage is cost. By preserving the building’s “bones”—the foundation, walls, and roof—you can sidestep the massive expense of demolition and ground-up construction. This can save you a fortune on materials and labor, directly padding your project's bottom line.

Beyond the upfront savings, adaptive reuse plugs directly into what the market wants right now:

- Sustainability: Today’s tenants, especially in office and multifamily spaces, actively seek out sustainable buildings. Repurposing a structure is about as green as it gets, slashing landfill waste and the carbon footprint that comes with new construction.

- Authenticity and Character: People are tired of cookie-cutter spaces. An old warehouse with exposed brick and original timber beams has a soul that a brand-new building can't fake. This "cool factor" often leads to premium rents and rock-solid occupancy.

- Faster Timelines: In many jurisdictions, an adaptive reuse project can get you to the finish line faster than a new build. That means you start collecting rent sooner, which is a huge win for your ROI.

Navigating Incentives And Tax Credits

Here’s where it gets really interesting. One of the biggest financial levers you can pull in adaptive reuse is tax incentives, especially for historic properties. These programs are specifically designed to encourage private investors to save and revitalize older buildings. Knowing how to use them is key.

The Federal Historic Preservation Tax Incentives program is the big one. It offers a 20% income tax credit for the certified rehabilitation of a historic, income-producing building. Let’s be clear: this isn't a deduction. It's a direct, dollar-for-dollar credit against your tax bill, which can completely change the math on a deal.

Think about it: on a $5 million rehab of a certified historic building, a 20% tax credit means you get $1 million back. That’s a game-changer. It can make a project that looked marginal on paper suddenly look incredibly profitable.

Of course, it’s not just free money. There’s a process. You need to get the building on the National Register of Historic Places and ensure your rehab work meets the Secretary of the Interior's Standards. This is why having an architect who knows this process inside and out is non-negotiable.

On top of that, many states and cities have their own historic tax credits and grants you can stack on top of the federal program. This layering of incentives is where the most skilled developers create incredible value, all while saving irreplaceable landmarks for the next generation.

Executing Flawless Due Diligence and Financing

Once you've zeroed in on a property and have a solid strategy in mind, the real work starts. This is where seasoned pros separate themselves from the amateurs, and it all comes down to two things: due diligence and financing. A great deal can completely fall apart at this stage, while a seemingly average one can turn into a home run with the right investigation and capital structure.

Think of due diligence less like a checklist and more like an investigation. You're the lead detective, and your mission is to uncover every single clue about the property’s past, present, and future. This is where you either confirm your initial assumptions or, more importantly, discover the hidden gremlins that could sink your entire investment.

This process is all about digging deep into the property's health. You have to validate every number, inspect every corner, and understand every legal document tied to the asset.

The Three Pillars of Property Investigation

Smart due diligence can be broken down into three key components. If you skimp on any one of these, you’re setting yourself up for a world of expensive surprises after closing.

Physical Due Diligence: This is the hands-on part. It means a thorough, top-to-bottom inspection of the building's physical condition—from the foundation right up to the roof. You'll bring in engineers and other specialists to assess structural integrity, HVAC systems, electrical, plumbing, and any potential environmental issues. Any deferred maintenance you find here isn't just a problem; it's a powerful negotiation tool.

Financial Due Diligence: Now it's time to put the seller’s claims under a microscope. This involves a deep audit of the rent rolls, verifying every line of the income statements, scrutinizing operating expenses, and reviewing each tenant lease. You're hunting for discrepancies, confirming the income stream's stability, and projecting future cash flow based on cold, hard facts—not the seller's rosy pro forma.

Legal Due Diligence: This piece is about diving into titles, surveys, zoning regulations, and service contracts. Is the title clean? Are there any hidden easements or encroachments that could kill your development plans? Does local zoning even permit your intended use? Answering these questions is your best defense against legal headaches that could derail your whole business plan.

A massive part of your financial homework is knowing how to accurately assess a property's worth. Mastering how to value a commercial property is non-negotiable for making smart investment decisions and ensuring you don't overpay.

Structuring the Right Capital Stack

Once your investigation confirms the deal is solid, the next mountain to climb is financing. The way you structure your capital stack—the mix of debt and equity you use to buy the property—is just as strategic as the investment itself. A well-designed stack minimizes your risk while maximizing your returns.

Sure, you can get a traditional senior loan from a bank, but the most successful CRE strategies often get creative with financing. This is especially true for value-add or adaptive reuse projects, where lenders might see a bit more risk.

The goal of creative financing isn't just to get the deal done; it's to align the capital with your specific business plan. The right structure provides the flexibility you need to execute renovations, lease up the property, and stabilize the asset.

Some of these alternative options include:

- Mezzanine Debt: This is a hybrid of debt and equity that slots in between your senior loan and your own cash. It's more expensive than a bank loan, but it’s a lot cheaper than giving away precious equity.

- Preferred Equity: This gives an investor a priority return on their capital—they get paid before you, the sponsor, see a dime. In exchange, they typically have no say in day-to-day operations.

- Joint Ventures (JVs): This means partnering with an individual or firm that brings the cash to the table. You provide the expertise and "sweat equity," they provide the capital, and you split the profits based on a pre-negotiated agreement.

The good news is that the financing landscape seems to be shifting in your favor. A broader sentiment shift shows that 69% of industry leaders expect financing to get easier this year, and 68% anticipate it will get cheaper. This optimism is fueled in part by a growing focus on sustainable projects, which are increasingly seen as more resilient and less risky. That's a huge tailwind for ambitious adaptive reuse projects that breathe new life into a building's infrastructure for the long haul.

Matching Your Strategy to the Right Property Sector

Having a killer investment strategy is one thing, but applying it to the wrong property type is like putting a brand-new engine in a car with four flat tires. You've got all the power, but you're not going anywhere. The best investors I know don't just master the how of a strategy; they're obsessed with the where. They meticulously align their approach with the property sectors best positioned to win in the current market.

This alignment is absolutely critical. Every property sector dances to its own beat, swayed by different economic drivers and demographic tides. A value-add plan that crushes it for a suburban apartment complex could completely fall apart if you tried the same thing on a Class B office building just down the street.

So, before you deploy a single dollar, you need to understand which sectors are attracting capital and, more importantly, why.

Targeting the High-Conviction Plays: Multifamily and Industrial

For the foreseeable future, multifamily and industrial properties are the undisputed darlings of the commercial real estate world. This isn't just a passing fad. It’s a direct response to deep, structural shifts in how we live and how we buy things. Both sectors offer a potent mix of steady demand and clear runways for creating value, making them a great fit for nearly any investment strategy.

The market has already voted with its checkbook. A 2025 survey showed that a whopping 75% of U.S. investors are actively hunting for multifamily deals. At the same time, 37% have their sights set on industrial and logistics properties.

And with 70% of investors saying they plan to buy more real estate in 2025 than they did in 2024, a wave of capital is heading straight for these two sectors. You can read the full analysis on investor sentiment to see how many are viewing today's pricing as a golden opportunity.

Putting Capital to Work in Apartments

Core and Core-Plus: The play here is to buy stabilized Class A or high-end Class B properties in growing submarkets. You're acquiring solid, cash-flowing assets and looking for small wins—light cosmetic upgrades to common areas or unit interiors that justify small, steady rent bumps over time.

Value-Add: This is where you roll up your sleeves. You're targeting older Class B or C apartment buildings that are tired, poorly managed, and have rents way below the market rate. The plan involves a heavy capital lift to renovate units, add modern amenities, and rebrand the entire property to attract a better tenant and command higher rents.

Seizing Opportunities in Logistics

Opportunistic: With e-commerce demand still roaring, ground-up development of modern distribution centers and last-mile fulfillment hubs near major cities remains a top-tier strategy.

Value-Add: Find an older, functionally obsolete warehouse—the kind with low ceilings or not enough loading docks—and bring it into the 21st century. This could mean literally raising the roof, punching in new dock doors, or reconfiguring the truck courts to handle modern logistics.

The key is to see these sectors not just as "safe bets," but as dynamic arenas where specific, well-executed commercial real estate investment strategies can unlock significant value. The demand is there; the challenge is to deliver the right product.

Finding Opportunity Where Others Aren't Looking

While everyone is chasing apartments and warehouses, savvy investors know that real opportunity often lies in sectors that are temporarily out of favor. Both retail and office, despite the negative headlines, have pockets of incredible value if you know where to look and aren't afraid to get creative.

Think about it: not all retail is dying. Grocery-anchored neighborhood centers are as resilient as ever. A great value-add play might be to buy a center where the anchor grocery store has a short-term lease, lock them into a new long-term deal, and then use that stability to attract better tenants for the smaller shops.

In the residential and hospitality space, understanding the nuances of short-term leasing apartments can give you a serious edge, turning a standard multifamily asset into a high-yield, flexible-stay property. And don't write off those underperforming office buildings. A well-located but empty office tower could be a prime candidate for adaptive reuse—think conversion to medical offices, apartments, or even a self-storage facility.

Bringing Your Investment Strategy to Life

A slick pro forma is one thing, but bringing a commercial real estate deal to life is where the real work begins. Even the sharpest investment strategies can fall apart if the on-the-ground execution—the actual design, permitting, and construction—isn't handled with expertise.

Success isn’t just about finding the right deal. It’s about navigating that deal through the gauntlet of design decisions and municipal approvals to create a profitable, physical asset. This is the phase where paper profits become brick-and-mortar reality, and every choice can either build or erode your returns.

Your Architect Is More Than a Designer; They're a Navigator

Choosing an architectural partner isn't like hiring any other vendor. Think of them as a crucial part of your investment team, one whose role goes way beyond just drawing up blueprints. They are your expert guide through the maze of local government regulations, a process that can easily sink a project if you don't know the terrain.

A good architect acts as the translator between your financial goals and the physical building. They’re the ones who will tackle the nitty-gritty of:

- Zoning and Land Use Rules: They make sure your project is compliant from the get-go, saving you from the nightmare of having to go back to the drawing board.

- Permitting and Approvals: They handle the submissions and back-and-forth with planning commissions and design review boards, which can be a bureaucratic headache for anyone unfamiliar with the process.

- Building and Energy Codes: They design a building that's not just up to code but is also safe, efficient, and durable for the long haul.

This kind of local knowledge is priceless. An architect who knows the ins and outs of the local planning department can spot potential roadblocks a mile away and steer your project clear, saving you an incredible amount of time and money.

How Smart Design Directly Impacts Your Bottom Line

Getting your plans approved is just the first step. Smart design is also one of the most powerful levers you can pull to maximize the long-term value of your investment. Every design choice has a direct financial impact, influencing everything from your operating expenses to how much tenants are willing to pay.

A well-designed building is simply a better-performing asset. It’s cheaper to run, attracts and keeps high-quality tenants, and holds its value far better over time by thinking ahead about future needs and environmental changes.

Let's break down how design choices translate into real dollars:

- Serious Energy Savings: Simple things like building orientation, high-performance windows, and modern HVAC systems can cut utility bills by 20-30% or even more. That savings goes straight to your Net Operating Income (NOI).

- Getting More from Your Site: A clever site plan can squeeze out more rentable square footage, create better parking and traffic flow, or add valuable outdoor amenities that tenants love.

- A Better Tenant Experience: It's no longer just about four walls and a roof. Thoughtful layouts, lots of natural light, and modern amenities are what today's tenants expect. Delivering on that means lower vacancy and the ability to command higher rents.

At the end of the day, turning a strategy into a successful reality means finding a partner who gets that great design isn’t an expense—it’s a fundamental driver of your financial success. By bringing that architectural expertise in early, you ensure the brilliant numbers on your spreadsheet become a profitable, tangible asset.

Frequently Asked Questions

What Is The Best CRE Investment Strategy For Beginners?

If you're just getting into the commercial real estate world, your best bet is to stick with Core or Core-Plus strategies. Think of a Core investment as the blue-chip stock of real estate—it's a stable, fully leased property that provides predictable cash flow with very little drama.

Core-Plus is the next logical step. You're still dealing with high-quality properties, but they have some minor, easy-to-fix issues that present a clear path to adding value. These approaches let you learn the ropes of the market without taking on the massive risks that come with ground-up development or speculative plays.

How Does Adaptive Reuse Compare Financially To New Construction?

From a financial standpoint, adaptive reuse often comes out ahead of new construction. You're typically looking at lower upfront costs because you get to keep the building's essential structure, which can also mean a much faster project timeline.

The real game-changer, though, is that adaptive reuse projects can unlock valuable historic preservation tax credits and other local incentives. These can dramatically lower your total investment, giving you a faster route to profitability with a unique, in-demand building.

When you find the right asset, it's an incredibly powerful way to create value.

How Important Is ESG In The CRE Investment Climate?

ESG—that’s Environmental, Social, and Governance—is no longer a "nice-to-have." It’s become a critical piece of the puzzle. Everyone from investors and lenders to the tenants themselves sees sustainable, energy-efficient buildings as safer, more valuable long-term assets.

It's simple, really. Properties with solid ESG credentials tend to pull in higher rents, attract better tenants, and run on lower operating costs. If you ignore ESG today, you risk facing hurdles with financing and could end up with a property that's worth less as the market continues to demand more sustainable buildings.

At Sherer Architects, LLC, we help turn ambitious commercial real estate investment strategies into tangible, profitable realities. Whether you're navigating the complexities of a historic preservation project or executing a challenging adaptive reuse, our team has the hands-on expertise to guide you from concept to completion.

Find out how we can help maximize your investment’s potential at https://shererarch.com.