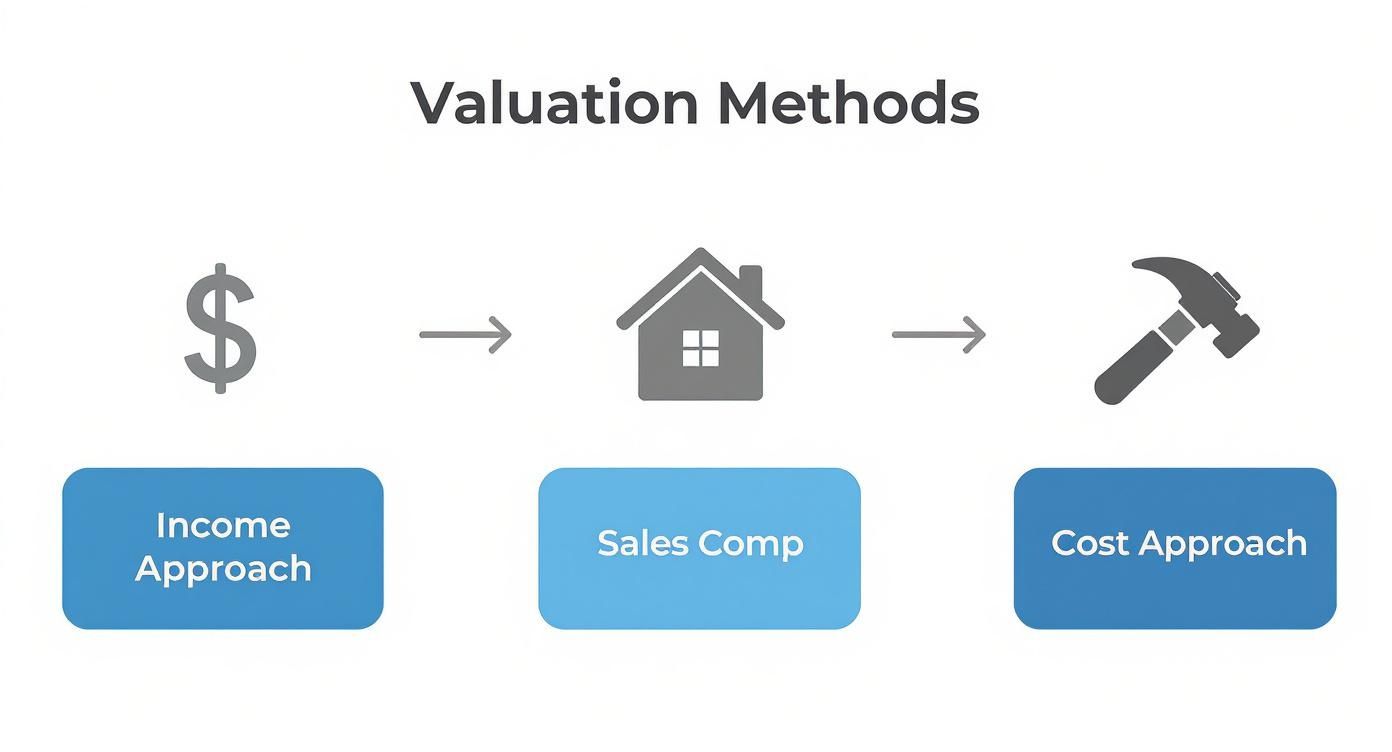

When you're trying to figure out what a commercial property is worth, it all comes down to three classic approaches: the Income Approach, the Sales Comparison Approach, and the Cost Approach. Think of these as different lenses to look through. Each one gives you a unique perspective on the property's value, and the one you lean on most heavily really depends on the building itself and what the market is doing.

This isn't just theory—it's the professional framework we use every day to build a solid financial case for a property's value.

Decoding the Three Core Valuation Methods

Before you even touch a calculator, it’s crucial to get the strategy right. Valuing commercial real estate isn’t like pricing a house where curb appeal and emotion can sway the number. Here, it’s almost entirely a financial equation. Your job is to pin down a value based on how much money the asset can make, what similar properties have recently sold for, or what it would cost to just build a new one from the ground up.

A seasoned appraiser or investor rarely bets the farm on a single method. The smart play is to use at least two, and often all three, to arrive at a more defensible and well-rounded valuation. The real skill is knowing which approach should carry the most weight.

Selecting the Right Valuation Tool

The property itself is your best guide. If you're looking at an office building or a shopping center with a roster of paying tenants, the Income Approach is your go-to. Its value is fundamentally tied to the cash it spins off month after month.

But what about a unique, owner-occupied warehouse with no rental income? In that case, you'd pivot to the Sales Comparison or Cost Approach. Since there's no income stream to analyze, your best bet is to look at what comparable industrial buildings have sold for or to calculate the cost to replace it.

To help you choose the best valuation path, we've summarized the core methods in this table.

Quick Guide to Commercial Property Valuation Methods

| Valuation Method | Best For | Key Metric or Principle |

|---|---|---|

| Income Approach | Income-producing properties (offices, retail, multifamily) with predictable cash flow. | Net Operating Income (NOI) and Capitalization Rate (Cap Rate) or Discounted Cash Flow (DCF). |

| Sales Comparison Approach | Most property types, especially owner-occupied or unique assets where good "comp" data is available. | Price per square foot or unit of recently sold, similar properties, adjusted for differences. |

| Cost Approach | New construction, unique-use properties (e.g., a school or church), or when checking insurance values. | The cost to build a replacement property from scratch, minus depreciation. |

Each method provides a distinct pathway to determining value, and understanding when to use each is the first step toward a reliable assessment.

This workflow is a great starting point for figuring out which method fits your situation.

As the infographic shows, you follow a different path depending on the property's characteristics. For a deeper dive into the nuts and bolts of each method, this guide on how to value commercial property is an excellent resource.

Key Takeaway: The most reliable valuations don't just pick one method; they triangulate a final value by considering the results from multiple approaches, giving more weight to the one that best fits the property type and available market data.

Finding Value with the Sales Comparison Approach

While running the numbers with the Income Approach gives you a solid look at a property's financial engine, sometimes the clearest picture of value comes from a much simpler question: what are similar properties actually selling for? This is the heart of the Sales Comparison Approach.

Think of it as grounding your valuation in reality. It's an intuitive method that mirrors how we price homes, but with a lot more nuance for commercial assets. We’re looking at real, closed transactions to see what buyers in the current market are willing to pay. It’s no wonder this is one of the most trusted methods out there; it directly reflects the pulse of the market. You can read more about the best commercial real estate valuation methods and see why this one is so popular with the pros.

Sourcing Reliable Comparable Sales Data

The whole process lives or dies by the quality of your "comps." Without solid, truly comparable sales data, your valuation is just a shot in the dark. The goal is to find properties that mirror yours in terms of use, size, location, and age.

So, where do you get this intel?

- Commercial Real Estate Databases: This is your first stop. Heavy-hitters like CoStar, LoopNet, and Crexi are the industry standard for a reason. They offer deep dives into closed deals, giving you the sale price, date, property specs, and sometimes even the players involved.

- Public Records: Don't overlook the county assessor's office. It’s a goldmine of raw data on recent sales. The information might not be as neatly packaged, but it's authoritative.

- Broker Networks: This is the "insider" source. Commercial brokers live and breathe this market. They hear about off-market deals and understand the story behind a sale—context you'll never find in a database. Building these relationships is one of the smartest things you can do.

As a rule of thumb, stick to sales from the last six to twelve months. A deal from two years ago is ancient history in a fast-moving market.

The Art of Making Adjustments

Here's the thing: you'll almost never find a perfect, identical comp. That's where the real skill comes in. You have to systematically adjust the sales price of each comparable property to account for its differences from your own. It's about creating a true apples-to-apples comparison.

The logic is simple. Your property is the baseline. If a comp is better in some way—say, a prime corner location or a brand-new roof—you make a negative adjustment to its sale price to bring it down to your property's level. If the comp is inferior—maybe it’s smaller or has a ton of deferred maintenance—you make a positive adjustment, bringing its value up.

Pro Tip: Document every single adjustment and your reasoning behind it. If you adjust for condition, note the specific issues. If you adjust for location, explain why. This paper trail is what makes your final valuation defensible, not just an opinion.

Key Factors for Adjustment

Adjustments aren't pulled from thin air. They’re calculated based on specific characteristics that drive value. These are the big ones you'll always be looking at:

- Location: Is the comp on a main thoroughfare while yours is on a side street? That's a huge factor. A retail spot on King Street in Charleston might easily warrant a 15-20% premium over a similar building just a few blocks off the beaten path.

- Physical Condition: A building that’s been recently updated is worth more than a fixer-upper. A great way to quantify this is to get real contractor bids for the work needed on the inferior property and add that cost back to its sale price.

- Size: You'll almost always need to adjust for square footage. It's a common market dynamic that larger properties tend to sell for a lower price per square foot. You need to analyze the data to figure out that curve for your specific market.

- Amenities and Features: Does one property have a 20-car dedicated parking lot while the other relies on the street? Does it have a modern loading dock, high ceilings, or unique historic features? Each of these differences has a tangible value.

- Market Conditions: If a comp sold six months ago when interest rates were lower and demand was higher, you'll likely need to apply a negative "time" adjustment to its price to reflect today's cooler market.

By zeroing in on the right comps and carefully thinking through each adjustment, the Sales Comparison Approach helps you build a powerful, market-driven case for a property’s true worth.

Mastering the Income Approach with NOI and Cap Rates

When you’re looking at a commercial property that generates rent—whether it’s a retail strip, an office building, or an apartment complex—its value really comes down to its financial performance. This is where the Income Approach comes in. It’s the method that translates a property's profitability directly into a market value. Frankly, it's the language investors speak because it cuts through the fluff and answers the most important question: how much money does this asset actually make?

This approach isn't about curb appeal; it's about what the financial statements tell you. It treats the property as a business, and its value is a direct reflection of its operational health.

Calculating Net Operating Income The Right Way

The entire Income Approach hinges on one critical number: Net Operating Income (NOI). This figure shows you the property's annual income after you've paid all the necessary operating bills but before you factor in mortgage payments or income taxes. Think of NOI as the pure, unadulterated profit the property itself generates.

Getting this number right is non-negotiable. Here's how we build it from the ground up.

First, you start with the Gross Potential Rent (GPR). This is the absolute maximum rent you could collect if the property were 100% occupied for the whole year, with every single tenant paying the full market rate.

Of course, no property stays full all the time. You have to account for reality by subtracting an allowance for vacancies and for tenants who don't pay. A market-standard vacancy rate is often between 5-10%, but this can swing wildly depending on the local market and the type of property you're dealing with.

Finally, you add in any other income. Don't forget the money from laundry machines, parking fees, or even billboard rentals. Tallying all this up gives you the Effective Gross Income (EGI). From there, you subtract your operating expenses.

What Counts as an Operating Expense?

This is where a lot of new investors get tripped up. Operating expenses are the day-to-day costs of keeping the lights on and the property running smoothly. They do not include your financing costs or major capital improvements.

Here’s a clear breakdown of what goes in and what stays out:

| Include in Operating Expenses | Exclude from Operating Expenses |

|---|---|

| Property Taxes | Debt Service (Mortgage Payments) |

| Property Insurance | Capital Expenditures (e.g., new roof) |

| Utilities (if owner-paid) | Tenant Improvements |

| Repairs & Maintenance | Depreciation |

| Property Management Fees | Income Taxes |

| Landscaping & Janitorial | Leasing Commissions |

Forgetting to exclude debt service is the single most common mistake I see. Your mortgage is unique to your financing deal, not a reflection of the property's intrinsic performance. If you include it, you’ll artificially tank the NOI and, as a result, the property's calculated value.

Expert Insight: Always, and I mean always, scrutinize the seller's expense list. Some owners might conveniently "forget" to include a line item for management fees if they manage it themselves, or they might understate repair costs. A proper due diligence process means verifying these numbers against market averages and, ideally, actual invoices.

Translating NOI into Value with the Capitalization Rate

Once you have a solid, defensible NOI, you need a way to turn that annual income stream into a total property value. This is where the capitalization rate (cap rate) comes into play. The cap rate is a simple but incredibly powerful ratio that reflects the expected rate of return on a real estate investment.

The formula is straightforward:

Property Value = Net Operating Income (NOI) / Capitalization Rate (Cap Rate)

A lower cap rate means a higher property value and is usually tied to lower-risk, stable assets in prime locations. On the flip side, a higher cap rate suggests higher risk but a potentially better return, often seen with older properties or those in up-and-coming neighborhoods.

So, where do you find the right cap rate?

- Recent Sales Data: Look at the NOI and sale prices of comparable properties that just sold in your market.

- Broker Reports: Commercial real estate brokers and big firms publish market reports all the time with average cap rates broken down by property type and area.

- Appraisal Data: Professional appraisers have access to proprietary databases that track these metrics with precision.

When you're weighing the potential returns, mastering the income approach is absolutely critical, especially if you're looking into an investment in an apartment complex. A tiny shift in the cap rate can have a massive impact on the final valuation, so getting this number right is the key to making a smart investment.

A Deeper Dive into Discounted Cash Flow Analysis

While a cap rate gives you a fantastic snapshot of a property's value based on a single year's income, it has its limits. The real world isn't static. Cap rates assume a property's income will cruise along without any changes, which we all know rarely happens.

For properties with a more complex financial future—think an office building with staggered lease renewals or a retail center planning a major expansion—you need a tool that can see around the corners. This is where Discounted Cash Flow (DCF) analysis really shines.

Think of DCF as building a multi-year financial movie of the property's life under your ownership, instead of just taking a single snapshot. It forces you to account for future rent hikes, planned capital projects, and changing operating expenses over a typical 5 to 10-year holding period.

This forward-looking approach is precisely why sophisticated investors lean on it for major decisions. The DCF method is widely considered the most detailed valuation approach because it directly incorporates the time value of money and captures a property's entire projected performance. You're not just looking at today; you're projecting future cash flows and then discounting them back to what they're worth in your pocket right now. For more on how this fits into the bigger picture, you can explore detailed insights on major methods for commercial real estate valuation.

Building Your Financial Projections

The heart of a DCF analysis is your proforma—a detailed forecast of the property’s Net Operating Income (NOI) for each year you plan to own it. This isn't just a copy-and-paste job of the current rent roll. You need to roll up your sleeves and make educated assumptions grounded in market data and the property's unique situation.

A solid projection model has to account for several key moving parts:

- Scheduled Rent Increases: Dig into the existing leases. Are there built-in rent escalations? Make sure you factor those bumps into the correct years.

- Market Rent Growth: What happens when leases expire? You'll need to project the new rents you can realistically achieve based on market trends. A 3% annual growth is a common starting point, but you must tailor this to your specific submarket.

- Vacancy Fluctuations: If a major tenant's lease is up in year three, you'd better model a temporary spike in vacancy and the costs to release that space.

- Operating Expense Inflation: Property taxes, insurance, and maintenance costs never seem to go down. It's standard practice to project these to increase annually, often by 2-3%.

Forecasting the Reversion Value

After projecting your annual cash flows, the next big piece is estimating what you'll sell the property for at the end of your holding period. In valuation lingo, this future sale price is called the reversion value or terminal value.

The most common way to pin this down is by applying a "terminal cap rate" to a future year's income. You take the NOI you've projected for the year after your holding period ends (so, Year 11 in a 10-year model) and divide it by an estimated future cap rate. This terminal cap rate is usually a bit higher than today's market rate to account for the building being older and other potential future risks.

Pro Tip: Your terminal cap rate assumption is one of the most powerful levers in a DCF model. A tiny tweak here can dramatically swing the final valuation. Always be prepared to defend why you chose a specific rate, often by pointing to historical cap rate trends for similar assets in the area.

Selecting the Right Discount Rate

Okay, so now you have a series of future cash flows: the annual NOI for each year plus that big reversion value at the end. But a dollar in ten years is worth less than a dollar today. The next crucial step is to bring all that future money back to its present-day value.

We do this using a discount rate. The discount rate is simply the annual return an investor would demand to take on the risk of this particular investment. It's a reflection of opportunity cost—if you didn't buy this property, what return could you get on another investment with a similar risk profile?

Choosing this rate is part art, part science. It’s influenced by a few key things:

- The interest rates on any loans you're getting.

- The perceived risk of the property itself and its market.

- The investor's own required rate of return, or "hurdle rate."

Once you've landed on a discount rate, you apply it to each year's projected cash flow. The sum of all those discounted cash flows is the property’s present value, according to your DCF model. It's a lot more work than a simple cap rate, but this granular approach gives you a much richer and more defensible understanding of what an asset is truly worth.

DCF vs Direct Capitalization: A Comparison

Both DCF and the direct capitalization (cap rate) method fall under the Income Approach, but they serve different purposes. Here's a quick breakdown to help you decide which tool is right for the job.

| Feature | Direct Capitalization (Cap Rate) | Discounted Cash Flow (DCF) |

|---|---|---|

| Time Horizon | A single point in time (based on one year's NOI). | Multi-year period (typically 5-10 years). |

| Income Assumption | Assumes stable, consistent income and expenses. | Accounts for variable cash flows over time. |

| Complexity | Simple and fast. Easy to calculate and understand. | Complex and time-consuming. Requires many assumptions. |

| Best For | Stabilized properties with predictable income streams (e.g., a fully leased NNN retail building). | Properties with irregular cash flows, planned capital improvements, or multiple lease expirations (e.g., a value-add office building). |

| Key Output | A single value based on current market sentiment. | A detailed valuation based on the property's entire projected financial life. |

Ultimately, using a simple cap rate is perfect for a quick analysis of a stable, straightforward property. But when you're dealing with a more complex asset or making a major investment decision, the detailed story that a DCF analysis tells you is indispensable.

Tying It All Together: Reconciliation and Final Due Diligence

You’ve run the numbers using the income, sales, and cost approaches. Now you have three different potential values. So, which one is right? The answer isn't to just average them out. The final step, what we call reconciliation, is more of an art than a science.

Think of yourself as a judge weighing evidence. Each valuation method is a key witness, but not all testimony is equally credible for every case. Your job is to decide which "witness" tells the most compelling and relevant story for the specific property you're analyzing.

Weighing the Evidence from Each Approach

So, how do you decide which method gets the most weight? It all comes down to the property itself and the quality of your data.

If you're looking at a bustling retail center with a long history of stable, long-term tenants, the Income Approach is your star witness. The property's value is fundamentally tied to the cash it generates, making this the most reliable indicator. You'd lean heavily on your cap rate or DCF analysis.

But what if the property is a unique, owner-occupied industrial building? Finding truly comparable sales might be next to impossible, making the Sales Comparison Approach less reliable. Here, you might give more weight to the Cost Approach, especially if the building isn't too old.

The Final Argument: Reconciliation is where you build your case for a final value. You need a clear, logical reason for your conclusion. For example, you might state: "The Income Approach gave us a value of $2.5 million, while the comps suggested $2.35 million. Given the property's rock-solid rent roll and the lack of truly apples-to-apples sales in the market, we are placing 80% of our confidence in the income-based value."

Shifting Gears to Due Diligence: From Spreadsheet to Reality

Getting to a reconciled number is a huge milestone, but don't pop the champagne just yet. A valuation is only as good as the assumptions it's built on. The final due diligence phase is where you get your hands dirty and verify everything.

This is your chance to confirm that the reality on the ground matches the numbers on your screen. It’s where you uncover the skeletons in the closet—the leaky roof the seller forgot to mention, or the anchor tenant who’s secretly planning to leave. Skipping this step is, without a doubt, one of the most expensive mistakes you can make in commercial real estate.

Your Must-Have Due Diligence Checklist

A thorough, systematic checklist is your best friend here. This isn’t a quick walkthrough; it’s a forensic audit of the property's physical, financial, and legal health.

Financial and Legal Deep Dive

- Verify the Rent Roll: Don't just glance at it. Compare every line item against the actual signed leases. Are there any hidden rent concessions or unusual clauses?

- Abstract Every Lease: Yes, every single one. You're hunting for key details: renewal options, expiration dates, specific expense reimbursement terms (NNN, for example), and any co-tenancy clauses that could spell disaster if a major tenant leaves.

- Audit the Financials: Get at least three years of operating statements. You're looking for red flags and trends. Did the seller suddenly slash the repair budget in the year leading up to the sale to make the NOI look better?

- Review Service Contracts: Look at every contract for landscaping, security, cleaning, and more. Can they be transferred to a new owner? Are the costs reasonable for the market?

Physical and Environmental Inspection

- Property Condition Assessment (PCA): This is non-negotiable. Hire a commercial building inspector or engineer to do a top-to-bottom review. Their report will be your roadmap for immediate repairs and future capital expenses, covering everything from the HVAC systems to the parking lot pavement.

- Environmental Site Assessment (ESA): A Phase I ESA is your first line of defense against environmental liabilities from past uses. Lenders will almost always require this to check for potential contamination.

- Zoning and Code Compliance: Head down to the local planning department or check their online portal. Confirm the current use is permitted under local zoning. Are there any proposed zoning changes that could help or hurt the property? Make sure the building is up to snuff on all fire, safety, and ADA codes.

Once you’ve completed this rigorous process, your valuation is no longer just a theoretical number. It's a battle-tested assessment you can stand behind, giving you the confidence to move forward knowing you’ve uncovered the real story behind the asset.

Answering Your Top Valuation Questions

Even with a solid grasp of the core methods, the valuation process always throws a few curveballs. Knowing how to handle these tricky situations is what really sets a professional analysis apart. I get asked a lot of questions, but a few come up time and time again from investors and owners.

Let's dive into some of the most common ones.

How Much Does a Professional Commercial Appraisal Cost?

There's no simple, flat fee for a formal appraisal. The cost is all over the map, driven mostly by the property’s size, type, and complexity.

A straightforward, single-tenant warehouse might run you $2,500 to $5,000. But for something much more complex—say, a historic downtown hotel or a sprawling regional shopping center—you're looking at a bill that could easily climb past $10,000. The appraiser's own experience and the level of detail you need in the final report also play a big role in the final price tag.

What Is the Difference Between Value and Price?

This is a big one. It's a fundamental concept that trips up a lot of people, but getting it right is crucial. "Value" and "price" are related, but they are definitely not the same thing.

- Value is what your analysis says a property should be worth. It’s the number you get after digging into the comps, running the numbers on the NOI, or building out a full DCF model. It's an educated, data-backed opinion.

- Price is what the property actually sells for. It’s the final, negotiated number that a buyer and seller shake hands on. It’s a fact.

A great valuation gets you close, but things happen. Market psychology, aggressive negotiations, or a seller in a tight spot can push the final price well above or below the calculated value.

A property’s value is an opinion based on facts and analysis; its price is a historical fact established by a transaction. Understanding both is key to making smart investment decisions.

How Do You Value a Vacant Commercial Property?

This is one of the toughest valuation puzzles out there. When a building is empty, there’s no income stream, which makes the Income Approach feel like pure guesswork. So, what do you do? You have to rely heavily on the other two methods.

The Sales Comparison Approach usually carries the most weight here. You’ll need to hunt down recent sales of similar vacant properties and make some sharp adjustments for things like location, condition, and marketability.

The Cost Approach also becomes surprisingly relevant, especially if the building is relatively new and hasn't depreciated much. You’re essentially asking, "What would it cost to build this today?"

You can still bring in the Income Approach, but you have to build a "pro forma" analysis. This means you project what the rental income and operating expenses would be if the property were leased up at today’s market rates. This gives you a stabilized, albeit hypothetical, NOI to work with.

How Often Should a Commercial Property Be Valued?

Honestly, it depends entirely on your goals. For your own internal books and performance tracking, most portfolio managers I know will run an informal valuation once a year. It's a good way to keep a pulse on how your assets are stacking up against the market.

However, you’ll absolutely need a formal, third-party appraisal for certain events:

- Financing or Refinancing: Lenders won't lend a dime without one.

- Buying or Selling: It establishes the baseline for any serious negotiation.

- Property Tax Appeals: A fresh appraisal is your best weapon to contest an assessment.

- Partnership Changes or Estate Planning: You need a concrete number for legal and financial filings.

In a market that’s moving quickly, checking in more often is never a bad idea.

At Sherer Architects, LLC, we believe that a building's true value lies not just in its numbers but in its potential. Whether you're considering a new commercial project, an adaptive reuse, or preserving a historic gem in South Carolina, our team provides the architectural expertise to maximize your investment's enduring worth. Let us help you bring structure to life by visiting https://shererarch.com.